Real Estate For Cash Flow

I look at things from a much different lens. So as usual, I don't think I'm in jeopardy of repeating anything.

What I'd like to do first is address the misconception that I've seen on this thread that somehow you have to make your money back on a property before you make a profit.

This might be one of the most ridiculous things I've ever heard.

If you buy a bond, stock, or gold do you not make a profit until your paid enough interest or dividends to recoup your initial investment?

As if the asset you purchased is worth nothing. Let's think about this.

You have 150k in the bank so your net worth is 150k…if you buy a 150k home is your net worth now 0? or is it still 150k?

If this were true, the IRS wouldn't tax your cash flow because “it's not profit.”

Bottom line: Ignore this nonsense.

If you buy cash flowing property then the positive cash flow is profit, just like the interest earned from a savings account is profit.

Would you buy for cash flow only? Unequivocally YES.

Here's why…My entire investment framework is buying assets “cheap” and selling them when they're “expensive.”

Sounds obvious but very few “investors” think this way. It's not to say we don't come to the same conclusions occasionally but the framework in which we analyze a deal is night and day.

The difference is most investors only have the confidence to buy when assets are already expensive in hopes they'll become more expensive.

Do this over the long term, especially now, when we're 40 years into an interest rate bull market, and you'll most likely have problems.

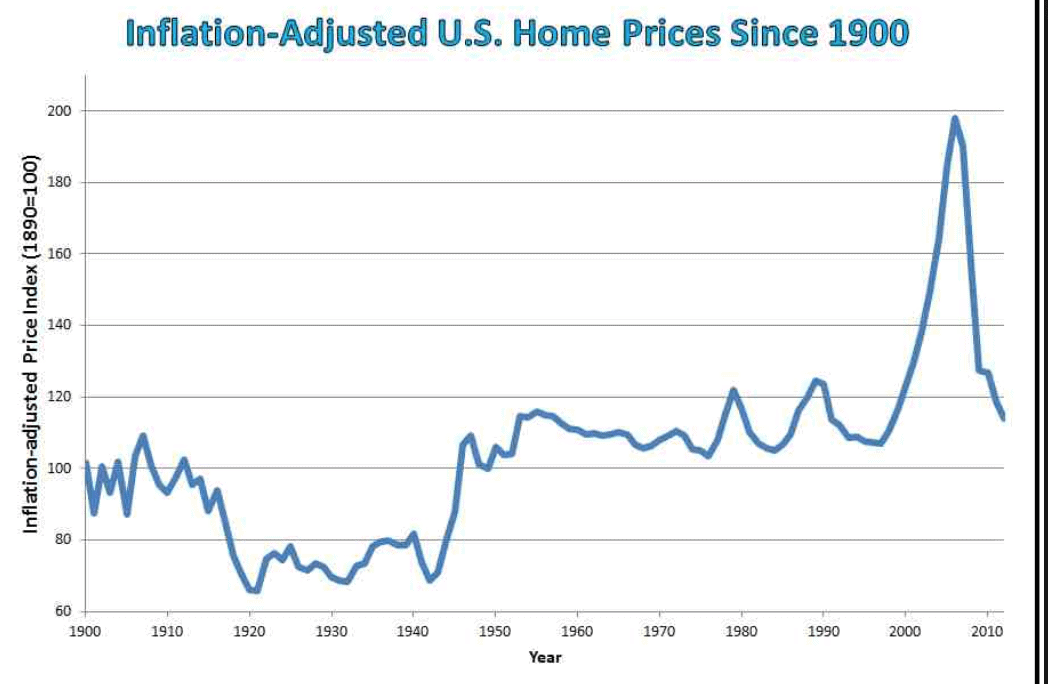

Back to the point. US housing, right now, on an inflation-adjusted, historical standard is expensive. Super expensive. But debt is historically cheap.

If, and this is huge if, you can buy cash flowing rental property, for under the cost of construction, using 30-year fixed rate debt, you've got tremendous positive asymmetry.

In other words, very limited downside and a huge upside. But not necessarily with the inflation-adjusted appreciation of the asset/property. see chart

So where is the probability high that you'll make money?

Or what I like to say, increase your purchasing power (accounts for inflation.)

Answer: On what you're buying that's cheap, the debt.

I know you talked about using cash…I'll address that later.

If you can lock in a rate of 4% over 30 years, at any point in the next 30 years, if inflation exceeds 4% there's a transfer of wealth from the issuer of the debt to you.

Said more simply, you make money.

But wait, there's more! 😉 You also make money on inflation itself, even if your asset only goes up with the rate of inflation.

NOTICE:

- You put 20k down on a 100k property

- The inflation rate is 10% one year

- The nominal price of your property goes to 110k, an increase of 10%

- 10k is 50% of the 20K you actually invested

So what we can see by this simple example is you gain purchasing power with inflation, as long as you use fixed-rate debt.

But that's just on the capital appreciation side of the coin, let's look at cash flow.

If your mortgage payment is $1000 (fixed) and your rents only go up with inflation.

Again, you make money. Take the extreme of the 1970s when inflation increased by 50% in 5 years.

Your mortgage is $1000 your rent is $2000, 5 years later your rent is $3000 but your mortgage is still $1000.

You gained 100% net cash flow (1000 – 2000 = 1000 and 1000 – 3000 = 2000) but inflation only went up by 50%.

Now let's consider the macro.

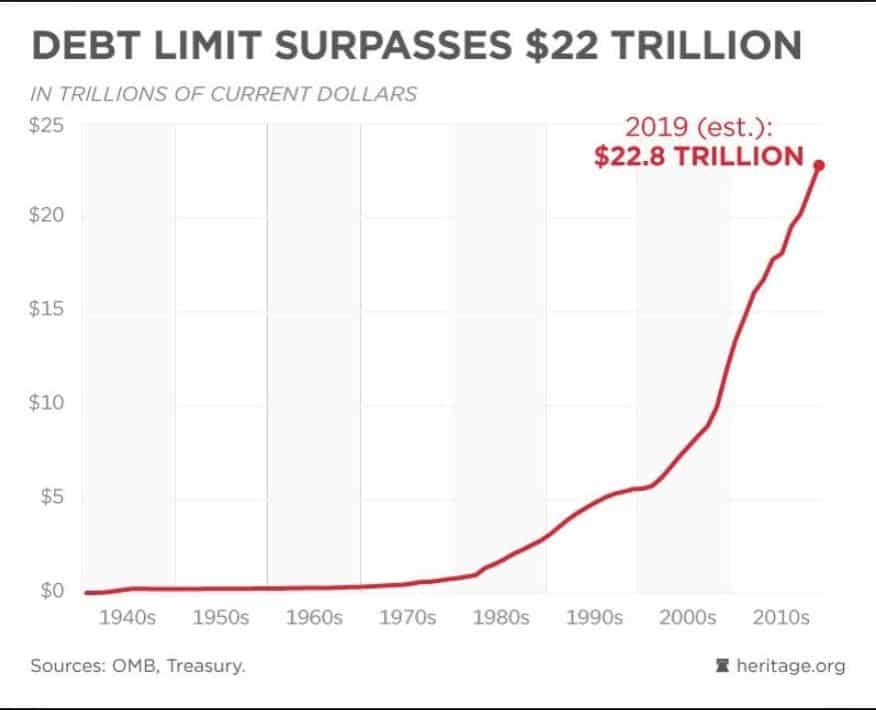

The US is almost 23 trillion in debt, and that's doesn't include off-balance-sheet debt such as social security and other unfunded liabilities, and currently, they're running trillion dollar+ annual deficits…and that's with a republican in the white house.

Throw a Dem in the white house in 2020 that drank the MMT (modern monetary theory) cool-aid and believes deficits don't matter, and the annual deficit could easily reach 2-3 trillion, or higher.

There are 2 ways out of a debt problem.

A. Default and

B. Inflation

This is why, whenever you hear Fed chair Powell talk, it's almost always about inflation targets.

Meaning they're actually trying to ensure inflation stays above a certain level!!

Will we see years of 10% inflation soon, like the 1970s? I don't know?

I never deal in certainties, only probabilities. And the probability is, because of these massive macro inflation tailwinds, we'll have more than 4% inflation over the next 30 years. Potentially way more.

So your upside is almost limitless, but what's your downside?

Again, assuming you buy, a single-family home, in a great neighborhood/school district, under the cost of construction, your biggest risk would be deflation.

If the CPI, more importantly, rents, go down nationally.

If this happens, everything I outlined above will work in reverse.

Rents go down, housing goes down, and your debt load stays the same. A transfer of wealth from the debtor to the creditor.

But this is where you've hedged your bet's by buying a starter home, preferably in a linear market (one without a lot of downward or upward swings), under the cost of construction.

It's pointed out often that there's an undersupply of homes under 200k, this is undeniable.

So buying this type of home, under construction costs, ensures that there will never be more supply of what you have unless prices rise to a level about construction costs.

SIDE NOTE: the big mistake investors are making now is they buy over the cost of construction, then you have much more downside.

With any strategy, there's downside risk. The key is asymmetry.

Ok, so that's my answer on why and how I'd invest for cash flow only.

Now let's think through using all cash…

The key here is the relative price where you buy.

There's a saying, “you make money on the buy-side.” I couldn't agree more.

Example: If you could somehow buy a property, with all cash, for 2012 prices, the expensive housing market is damned.

I know this is probably unrealistic, but again as long as you're buying a starter home under the cost of construction, it's a good way to preserve wealth and create a retirement plan.

Which sounds like it is your goal.

Going back to the inflation scenario, that in my opinion is most probable, real estate historically does very well. Not just in the US but globally.

Comparing bonds and a starter home rental property…

This is the no brainer of all no brainers.

Assume you agree with me that inflation over the next 30 years is the base case.

As I discussed earlier, inflation, above the rate of interest, is a transfer of wealth from the creditor to the debtor.

In other words, you want to be a debtor.

SIDE NOTE: The US is the largest debtor nation in the history of civilization. #inflation

And as a bondholder, you are the creditor, not the debtor.

Making matters worse, my guess is you wouldn't even get an interest rate that's above the Fed's target inflation rate. Meaning there's a 99% chance you lose money.

What happens if interest rates go up?

Remember, we're 40 years into an interest rate bull market.

In other words, interest rates have gone down for 40 years and interest rates are cyclical.

As you probably know the value of a bond has an inverse relationship to interest rates. Interest rates go up the value of your bond goes down.

So in summary, buying a bond gives you a near 100% chance of losing money because you'll be paid back with dollars that are worth less…and maybe even worthless…depending on inflation! 😉

Then to add insult to injury, the value of the bonds will to down in nominal terms as well, if interest rates go above the 5000-year worldwide lows.

Don't buy bonds…lol

Anyone have any more questions please don't hesitate to find me on social media. Links are in my profile description.

George

Comments are closed.