Limitless Government Bailouts?

The Fed’s alphabet soup type solutions have grown in size, and so did their quantitative easing commitment taking them to infinity and beyond.

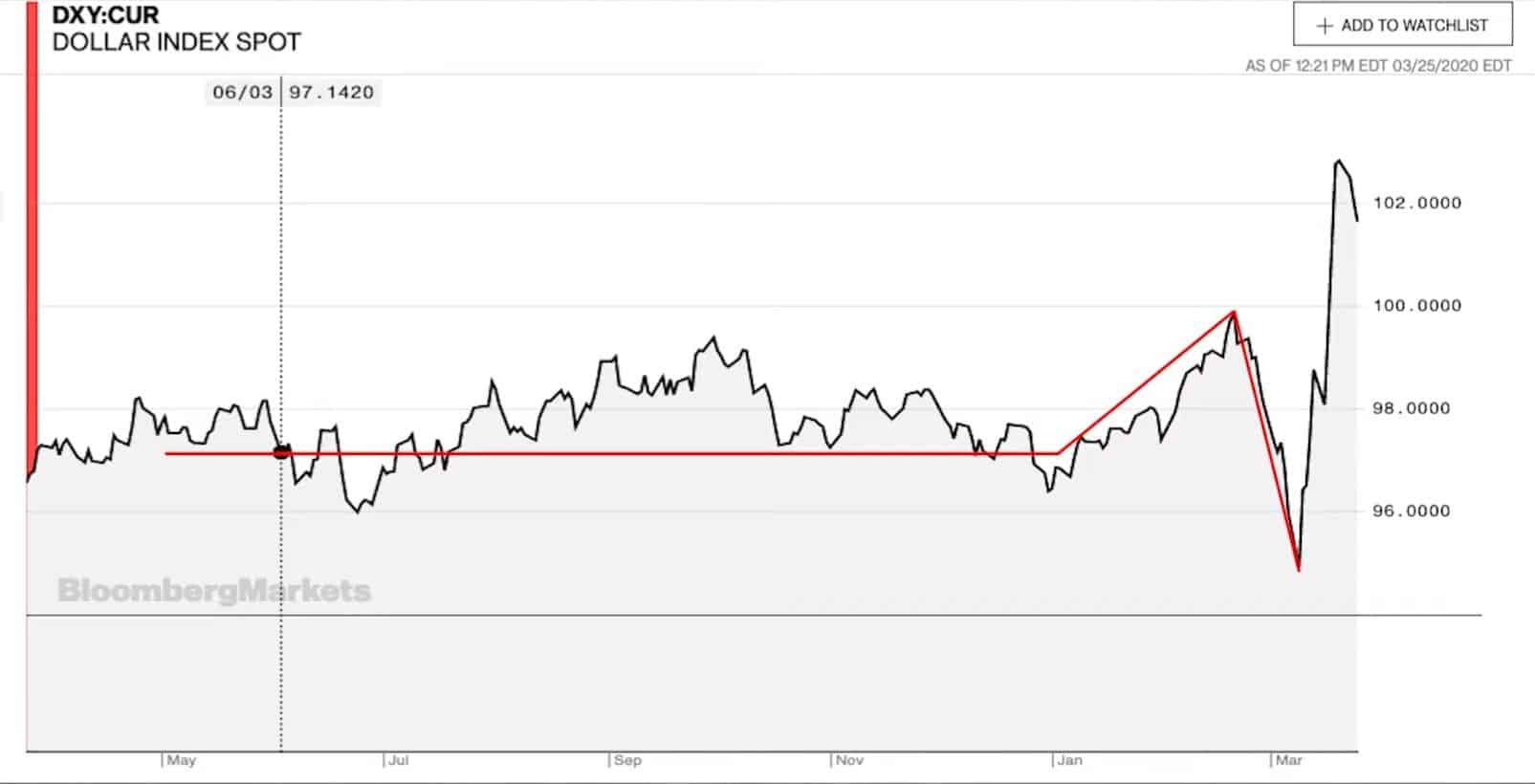

The dollar has skyrocketed for the last few weeks and there’s still no vaccine for the Covid-19.

A lot of questions arise due to the situation, and one of them is will the dollar be doomed?

My quick answer: No.

Not in the short term.

But before I get further into the dollar and how money is created along with Brent Johnson’s view of the rising dollar, I will go through the Fed’s four new programs and explain them to give you a better context of the situation.

Fed’s solution bailouts and QE

These programs are all about propping up the credit markets to make sure no one goes out of business by borrowing as much money as they want, but before we dive in, I will give you a context.

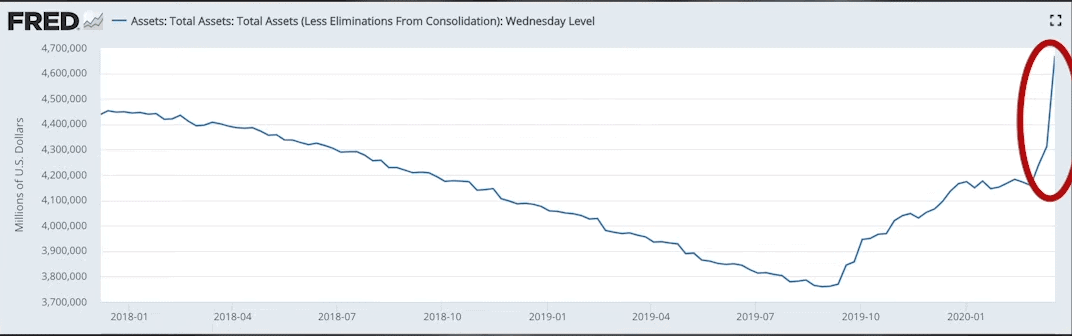

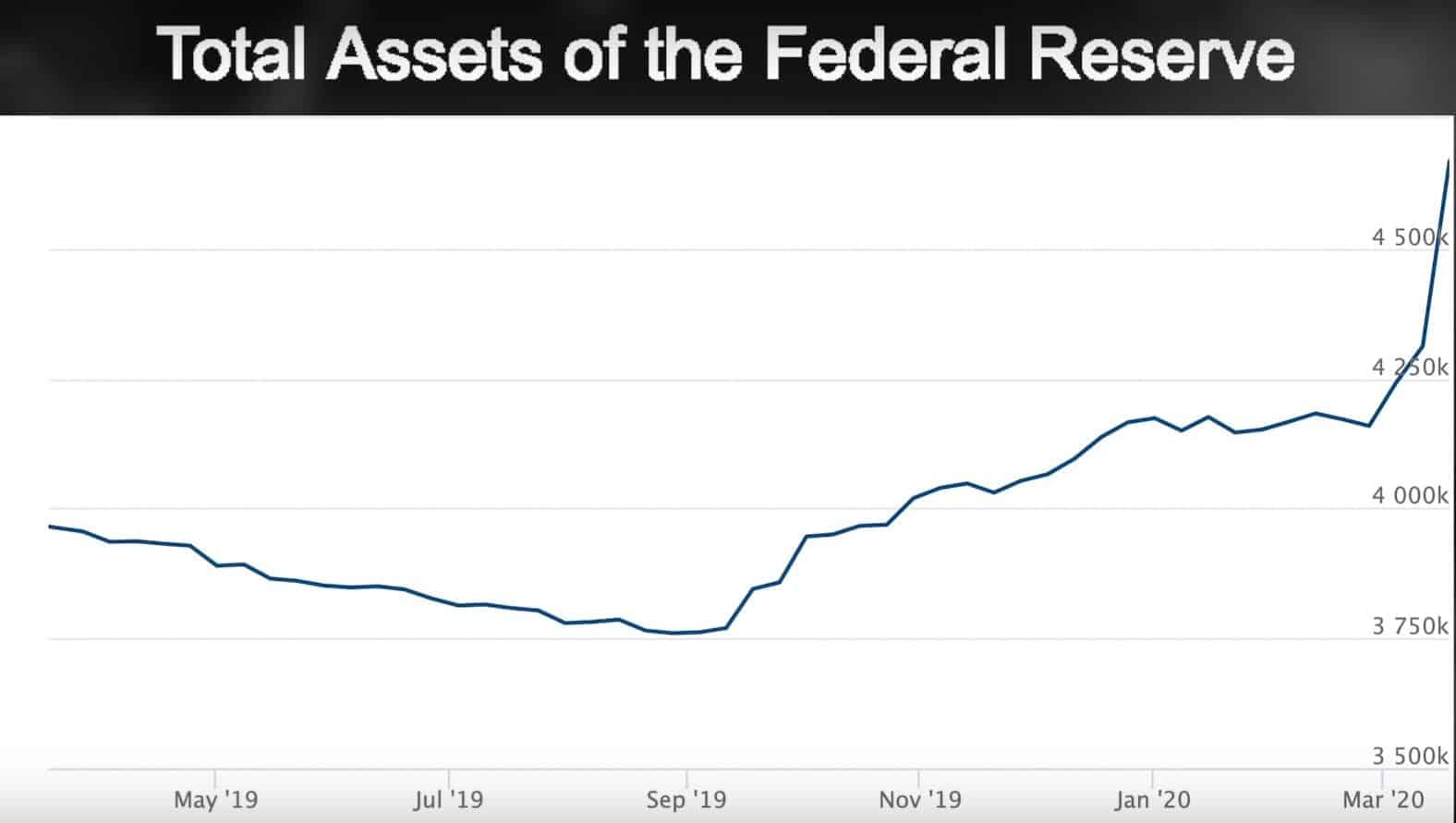

The Fed used to be in quantitative tightening, as shown in the image, this means they were reducing the size of their balance sheet until they couldn’t because the repo market blew up on September 17th.

Because of it, the Fed started to increase its balance sheet by buying $60 billion a month worth of T-Bills, and making $700 billion of quantitative easing, however, they recently announced they will do an additional $125 billion a day of QE.

$125 billion in addition to the $700 billion they were already doing!

The Fed’s balance sheet is growing with the exact same type of curve you see in the cases of Covid-19 in the United States, exponentially.

Federal Reserve Unleashes Extensive Measures To Paper Over Everything

Every single day the Fed is coming up with more of these alphabet soup type solutions to bluntly throw at the problem and hope something sticks.

In my last blog, I went over some of the solutions the Fed is offering: the PDCF, the MMLF, and the CPFF, but since then, they’ve grown in size and number, which is why I’ll go over the old and new ones.

The extensive new measures the Federal Reserve has announced to support the economy are the PMCCF, the SMCCF, the TALF, and the ESF.

The Primary Market Corporate Credit Facility (PMCCF) is, simply put, the Fed printing up funny money and lending it directly to the corporations, instead of having to go through the primary dealers.

Looking at its fine print, the Fed considers this is a bridge loan for four years, and in addition to this, borrowers may elect to defer interest and principal payments during the six months of the loan, extendable at the discretion of the Fed.

Please read again.

The Federal Reserve is admitting they’re giving this money to corporations. This is 100% a bailout.

The Secondary Market Corporate Credit Facility (SMCCF), in other words, is the Fed taking its money, going directly to the corporate bond market and buying the existing debt.

Again, not having to go through the primary dealers in order to keep interest rates low.

Term Asset-Backed Securities Loan Facility (TALF), will enable the issuance of asset-backed securities backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration, and certain other assets.

This means the Fed is going directly into the market to buy these assets in exchange for non-recourse loans.

In other words, the Fed’s printing the funny money and gifting it to investors in hopes they buy the garbage debt, and why wouldn’t they with a non- recourse loan?

Why this is important!

This type of loan is important because no bank would issue such debt in the first place if they had to keep the paper or the loan on their books.

This means they’re not going to find a subprime borrower and give him $50,000 for the next ten years at 0% interest rate so he can buy a brand new Ford pickup truck that depreciates by 60% the second he drives it off the lot.

The borrow will default on that 100% guaranteed, so before the ink is dry, the bank will sell the debt to Wall Street, who bundles up all the toxic garbage like mortgage-backed securities and pawns them off on any pension fund.

If they can’t find a pension fund who would take it, then this means there won’t be more student loans, auto loans, credit cards or SBA loans.

You can imagine what will that do to the economy?

The Fed needs to find a pension fund and give them free non-recourse money to make sure the credit is continually flowing and the debt keeps growing.

Why? Remember the economy is built on asset prices, debt, and confidence.

Moving on to the measures I explained in my last article, the MMLF, was modified by adding to it a Variable Rate Demand Notes (VRDNs), which means they’re expanding what they’re buying to municipal variable demand notes and bank certificates of deposit.

The Fed also modified the Commercial Paper Funding Facility (CPFF) by including high quality and tax-exempt commercial papers as eligible securities and lowering the interest rates they were charging the corporations with.

Lastly, as I said before, all of these programs are about propping up the credit markets making sure no one goes out of business because they can just borrow as much money as they want.

But its also about taking the assets off the balance of the private sector and moving them onto the Fed’s balance sheet so nobody has to take a haircut.

Now, on the other hand, the government doesn’t want to be undone by any means.

They also came out with their $2 trillion stimulus package, and they’re going to make it rain on the entire economy.

What’s bizarre to me is the Fed is stepping in and bailing out everybody, yet, the government is starting to do that as well.

What’s the second bailout for?

It seems like its a corporate charity at the expense of the taxpayers because they’re giving them profits at the expense of our futures, our children’s futures, and even our grandchildren’s future.

They are giving it in the form of running up all the deficits that will be required to pay this debt and even the interest on the debt, but what if the debt goes to 40, 50, 100 trillion dollars?

Think about what the interest of this debt is going to be, then, also think about how the Fed is going to monetize it, and how much purchasing power will your next three generations lose on a moving forward basis?

Also, $1,200 are going to most individuals for four months, who on earth at the end of the fourth month is going to want to give up the $1,200?

Nobody.

This temporary program, like all temporary government programs, is going to become permanent. This is the art of the MMT and helicopter money I’ve been talking about for months.

Also, there’s a message that limits the future buybacks for corporate America, at least for the people who are taking these bailouts, which at the end of the day will most likely be everyone on the S&P500, even the Subway down the street.

Notice they’re saying no to the bailouts or at least they’re limiting them extensively.

Look at the flip side of the coin, if there are no corporate buybacks, there’s a very low probability the market recovers.

Why?

Because corporate buybacks have been the majority increase in the S&P500 for the last ten years.

This means if you have a 401(k), and you’ve taken a 50% hit over the last 30 days, you’re purchasing power has been cut in half, so if the market doesn’t recover, your purchasing power won’t either.

For a lot of baby boomers who are retiring right now, it means their purchasing power went down for 50% for the rest of their lives.

Now, with this context, let's dive into the dollar.

Is The dollar doomed?

No, at least not in the short term according to Brent Johnson, author of The Dollar Milkshake Theory.

Why?

In order to answer that question, we first need to understand his explanation of how money works.

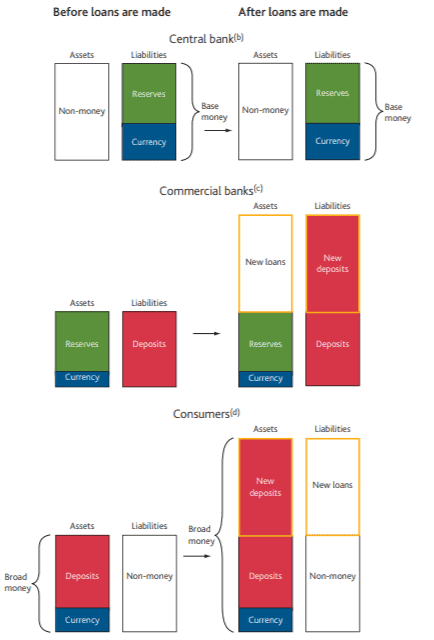

“Money is created in two ways, you can print it physically or add to the stock of the monetary base which frees up the ability to loan more. So you can either print it or loan it, those are the two methods via which money gets created.

This means that when you reach the end of the loaning, or you get a credit card contraction, money is being destroyed.

When loans aren’t being rolled over, money is no longer being created through expansion.

The only way to get new money into the system, to plug the hole, is by the Fed coming in and printing money or doing QE”.

how money works

Brent continues to affirm and conclude the problem with this is the hole is too big and the Fed can’t keep up with it even if they buy trillions of dollars a day.

This diagram from the Bank of England where they also explain how money is created illustrates Brent Johnson’s point very well.

We have three balance sheets here, the first one its the central bank’s balance sheet, the second one is from the commercial banks and the third one, consumers.

On the left-hand side we have everything before the loan is created, and on the right-hand side after the loan’s been created.

Please notice the red box on the left-hand side in the middle. Those deposits, which are liabilities for the commercial banks are the money supply.

So whenever a consumer goes to a commercial bank to borrow money for a home, for example, the bank creates more deposits for that consumer, and on the asset side of their balance sheet, they will now have their loan.

Let’s imagine the new loan is for $1,000, and prior to the new loan being created, there were $500 in the system, so now, after the loan, there’s $1,500 worth of money supply.

If the consumer immediately paid off the loan, they’d go from $1,500 of money supply right back to where we started, with $500, plus, they’re going to pay interest.

This is where it gets interesting, if the original loan amount was $1,000, let’s say they paid an additional $1,000 in interest over the lifespan of the loan.

This means that in order for the borrower to pay back the loan plus the interest rate he/she needs $2,000.

But remember there are only $1,500 dollars in the entire system, which means there aren’t enough dollars for them to pay back the loan with interest unless there’s more debt created increasing the number of dollars.

If so, the consumer would have the dollars to not only pay back the principal payments but the interest.

Finally, what does all of this have to do with the dollar?

Well, there’s a relation between the Federal Reserve’s balance sheet and the DXY, and it’s very easy to notice it when we compare the DXY chart and the Fed’s balance sheet chart.

Take a look.

This is why it’s so important to grasp how money is created and destroyed because once you do, it’s easier to comprehend why the dollar is going up and why it most likely won’t collapse in the short term.

Brent Johnson's dollar view

We already know how money is created and destroyed, which means we get the fact that there’s a fewer amount of dollars compared to the amount of debt and interest in the system.

Yet, I want us to go deeper into why Brent Johnson thinks the dollar will not be doomed in the short term.

He thinks the dollar will keep on going up to infinity and beyond, and before I unpack this, I want to clarify something.

Although we have, let’s say $20 of debt and interest in the system, we can pay it back with only $10 of the money supply.

Just because there is more debt and interest in the system, compared to the money supply, it doesn’t mean it can’t be paid off. We can do so just as long as the velocity stays high.

Velocity is the rate at which the currency circulates within the local economy, meaning how fast does it go from entity A to entity B.

The problem with this and Brent Johnson’s point with it is, because of the Covid-19, we can see velocity in the United States, and around the world come into a screeching halt, and to make matters worse we could see the new and additional loans or the new money supply coming to a stop.

Why?

Because people are not leaving their houses and are afraid of doing anything, except sit on the couch and watch Netflix, which leads them to refuse on taking any more debt while paying the existing debts they have along with not spending much money.

No more loans mean no more money supply.

All of this brings velocity down.

I will give you one more example.

If the United States had $2,000 worth of debt, and $1,000 worth of money supply, kind of a 2 to 1 ratio and some man called Fred paid $999, the money supply would go down to one.

However, the demand will still be $1,001.

The demand would skyrocket and so would the value of the dollar relative to the stuff in the local economy, goods and services, and the currencies outside the United States.

The Fed would now come and try to plug the hole by creating the additional $999 that were lost by Fred paying down his principal, and their previous problem is eliminated by them not having to go through the primary dealers.

With the new alphabet soup, the Fed circumnavigates the primary dealers so they can create deposits directly into the economy, this could give them the ability or a much better ability to create the $999 they need to fill the gap.

Despite this, Brent Johnson thinks the Fed isn’t going to be able to create money supply faster than the destruction of it by the individuals in the local economy and the whole United States going into a recession or depression.

He also talks about a great analogy using the musical chairs and the national debt of the United States.

The musical chairs game consists of people dancing around a limited amount of chairs while the music is playing, but when the music stops, everyone looks for a chair to be seated, if not, they’ll lose.

The analogy is, there are 23 persons in the room playing this game, each one of them represents a trillion-dollar of debt, so as a whole they represent the $23 trillion national debt.

However, they only have $4 trillion of base money at the Fed, which means that’s the real money they have to pay back all the debt ($23 trillion).

The musical chairs game represents velocity, so as long as the music is playing and all people are dancing around the chairs, there’s no problem.

But as soon as the velocity stops, meaning as soon as the additional money supply stops, everyone scrambles for a seat, 23 people will be looking for a chair while there are only four.

This analogy made me question myself and ask him, does the Fed have the ability to create another 23 chairs or the amount needed?

His answer was: Yes, they absolutely can, but it boils down to political capital.

He doesn’t think that when you look at the politics involved, regarding the psychology and the game theory, everything that goes into making those decisions, are going to have the ability to create more money to counterbalance the money that was destroyed in and outside the U.S.

I know this sounds crazy, but its what all of this boils down to, and I want to point out the fact that the difference between a Peter Schiff, Brent Johnson, Luke Grohman or Jim Records, isn’t how they analyze the system.

They all would all agree on how money is created, how it gets to the real economy and how it’s destroyed by people paying their current debts.

But what they disagree on is the distribution mechanism and the psychology involved with the participants in control.

If you get Brent and Luke talking side by side they’re going to agree on 99% of what they say, its the 1% of the unknown they disagree on.

I hope you got a better understanding of Brent Johnson’s Dollar Milkshake Theory, and to be clear what I’ve explained is not all of it, instead, I outlined some of the details and got into the nuance.