You can Profit From Inflation

In this article, you’re going to discover three different ways to profit from inflation nobody's talking about.

With these, you can make money from inflation and compound year after year.

I’m also going to explain where to use these strategies and where not to.

It’s incredibly important you understand where to use them, so keep reading.

All three methods have one thing in common: 30-year fixed-rate debt.

A 30-year mortgage does not exist in a free market

This may shock the Americans that think a 30-year mortgage is normal, but it does not exist outside of the United States of America.

This type of debt exists because it’s subsidized by the taxpayers and our government.

The reason it’s subsidized is the banks are almost guaranteed to lose money on this type of loan.

Therefore, if the banks are guaranteed to lose money, you are guaranteed to make money.

Let’s start diving into how to make money from inflation.

Method #1 (short-term gains) – Shorting the Dollar with 30-Year Fixed-Rate Debt

Buy a property with a 30-year fixed-rate debt and you will see short-term gains if the property goes up just with the rate of inflation.

Here’s how:

Let’s say we're talking about you, a very sophisticated investor, and you're going to buy a $100k house.

To buy the house you will have to give a $20,000 down payment, and in the first year of you owning the home, let’s pretend inflation goes up by the rate of 10%.

The 10% increases the price of the house, but it does not increase the value of it, because remember, it has gone up with inflation.

It only increases the price of your home to $110,000.

I’m going to restate this one more time, the house by itself has no more purchasing power.

It can’t buy any more goods or services.

Also, remember, you spent $20,000 on the down payment, so your cost basis is only $20k.

The price of the house went up by $10,000 so you have to add the 10% to the $20,000 you have already invested, and when you do so you get additional purchasing power above and beyond the rate of inflation.

I will explain a little bit further: if your $20,000 would have increased with the rate of inflation, you would have earned just $2,000, but you have an additional $10,000, because of your investment.

This means the spread is purchasing power or ROI you get on your $20,000, just for the value, or the price, of the home going up with the rate of inflation.

There's been no appreciation here, no real gains in the price of the house itself, but you have almost gained 50% on the amount of money you have in the house.

Method #2 (long-term gains) – Shorting the Dollar with 30-Year Fixed-Rate Debt

Buy a property with a 30-year fixed-rate debt and get long-term gains. In order for you to understand this better, I will briefly go through how inflation works.

How inflation works

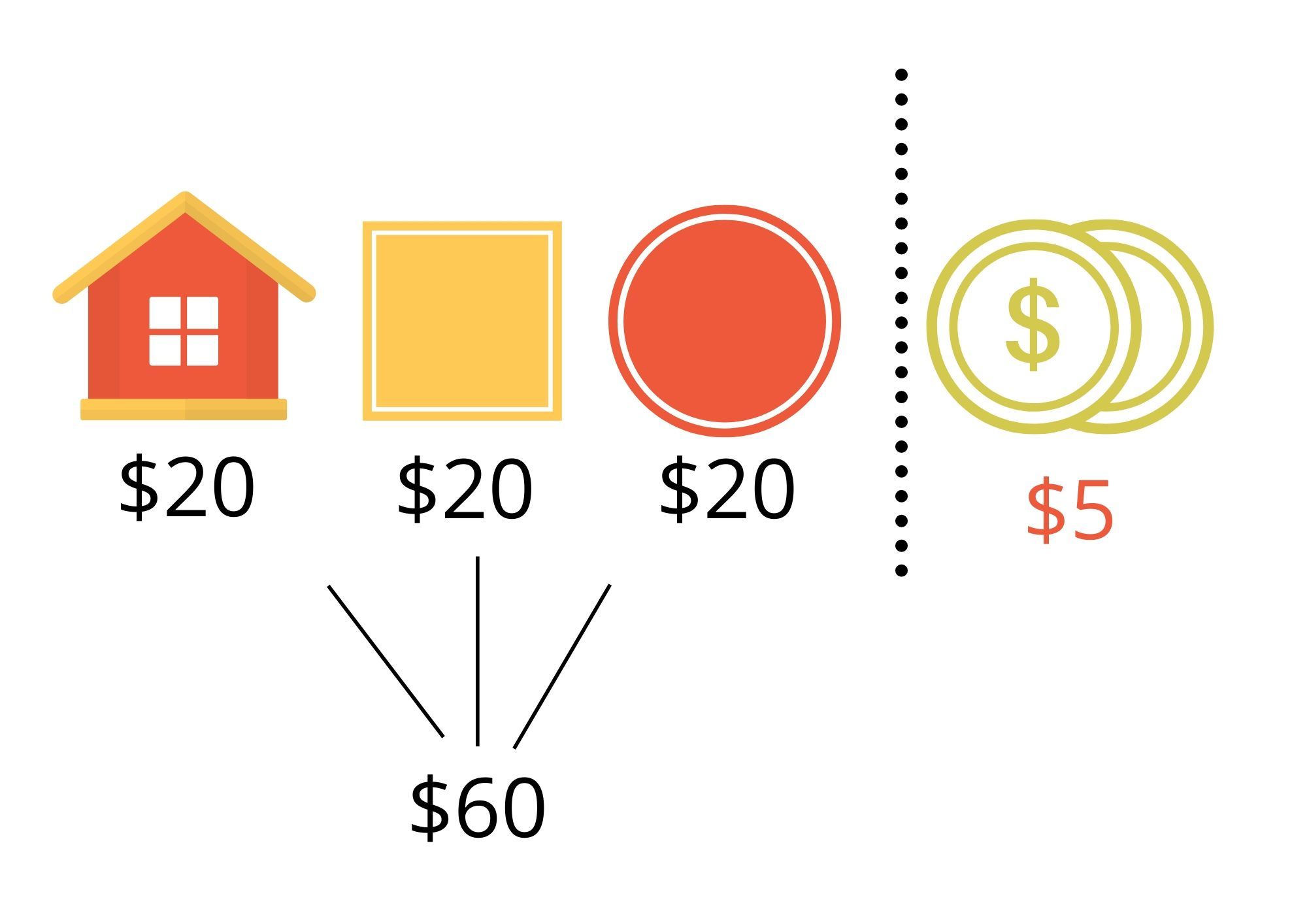

Here we have a house, in the image above, the square next to it represents the cost of goods and services like food, education, transportation, and healthcare.

The circle is your income, and on the right side is your loan, with a value of $5. Again, fixed-rate, this means it does not go up or down.

Let’s pretend for this example there’s only $60 in the entire world, so your home cost is $20, the cost of all these goods and services is $20, and your income is $20.

If I put my hat that says “Federal Reserve” and double the money to a hundred and twenty dollars, what is going to happen to the price of this home, goods and services, and your income?

Naturally, it will double, the price of your home will go to $40, as well as the goods and services, and your income.

You may think: “well, that’s great, my income just doubled!”

Yes! But it doesn’t matter because the cost of everything else also doubled.

But see, your loan is still $5, it’s the only thing that didn’t double.

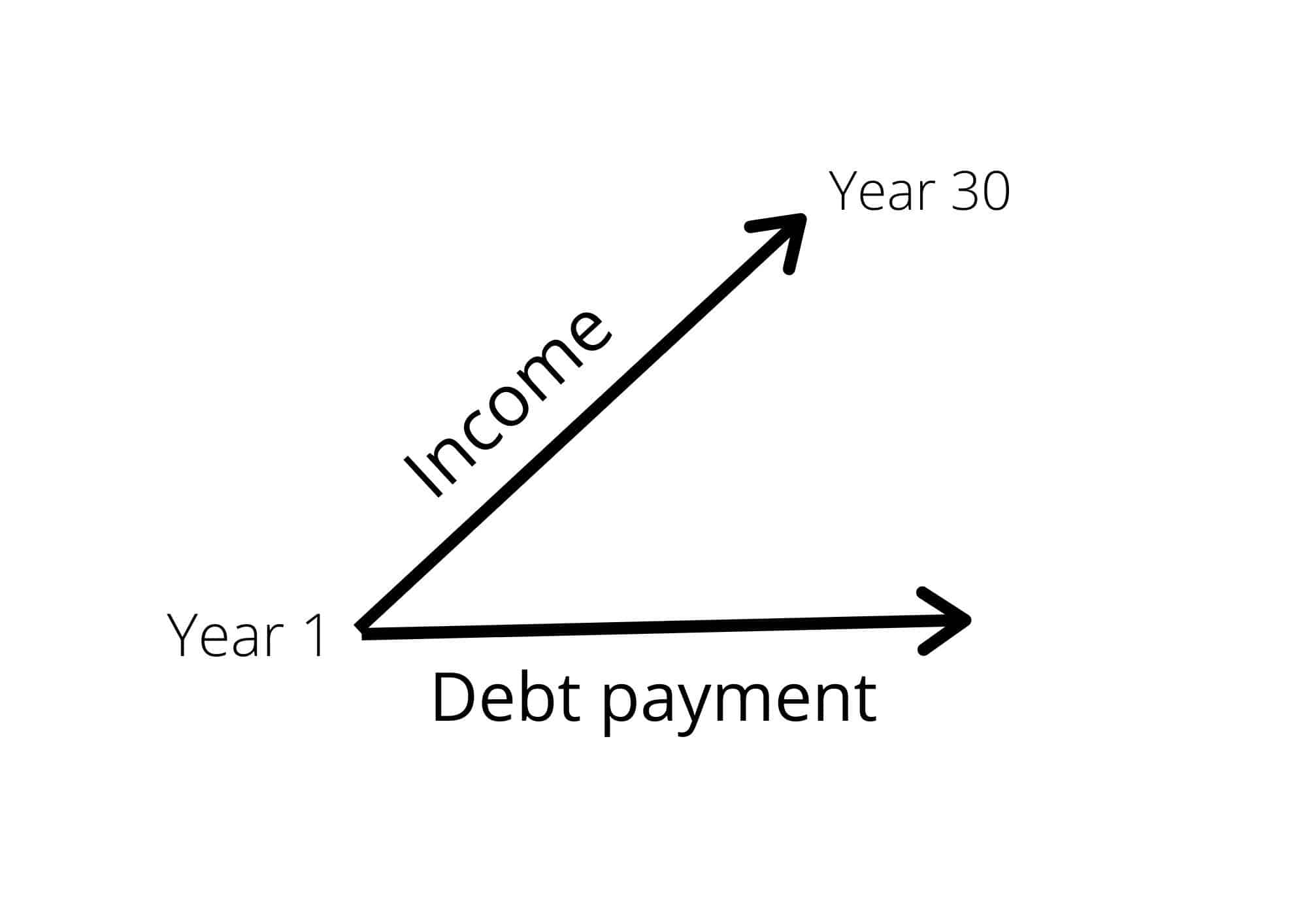

How Income Works When Leveraging A 30-Year Mortgage

Now, look at the image below in order to understand how your income works in this case.

It starts right here in year one, which I am pointing at, and goes all the way up to year 30.

It’s important to keep in mind, just like I said before because your income is going up, it doesn’t mean you can buy more things.

It doesn’t mean you are richer either, it just means your income is staying consistent with inflation.

Now, think of your debt payments.

Even though inflation is going up and up every year, your debt payments stay the same.

The discrepancy or the difference, between your debt payments and your income, is money in your pocket, in other words, purchasing power.

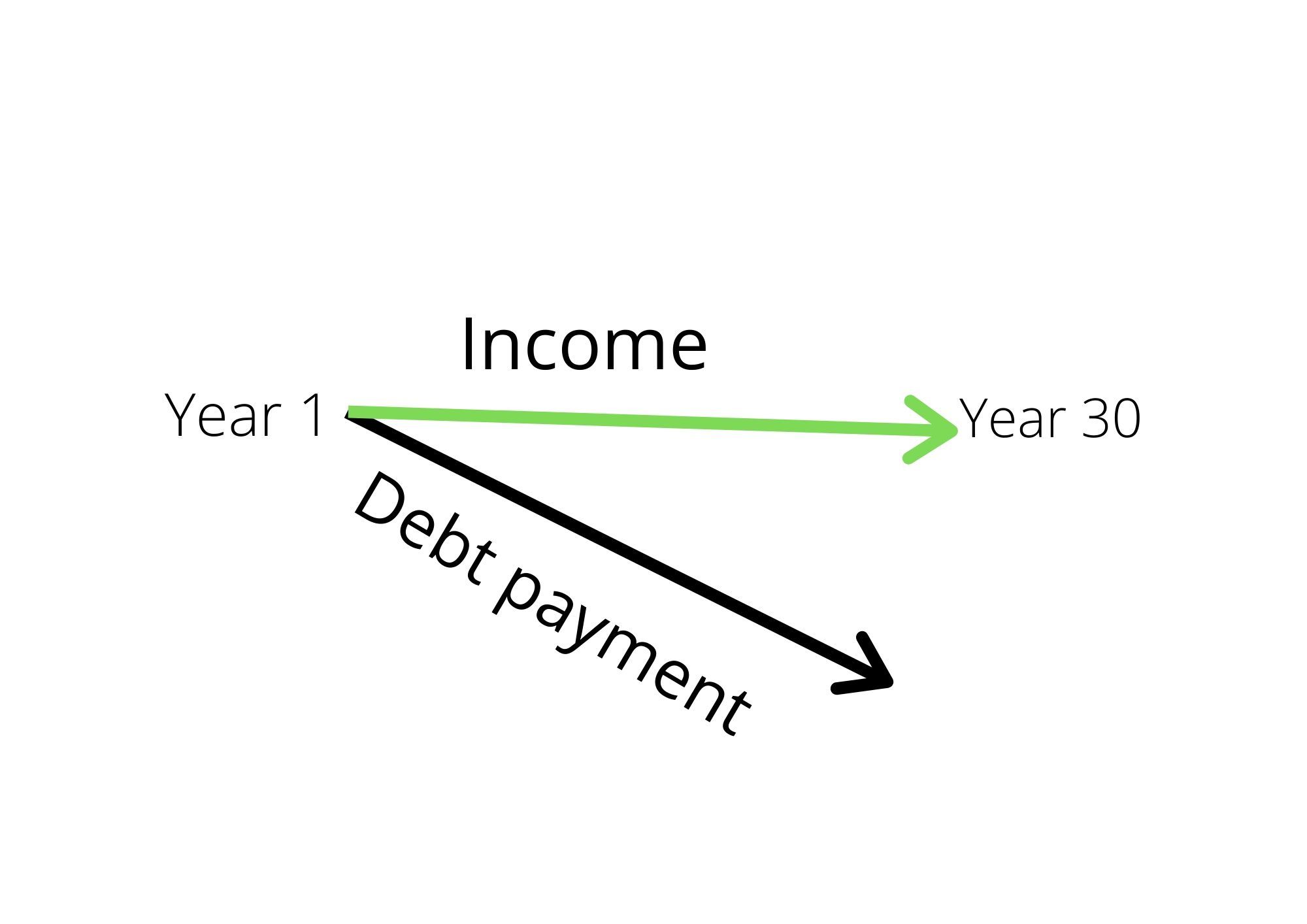

This example will make even more sense to you if I flip the figure I used in the previous picture, upside down, as shown in the image.

The green line is your income.

I like it when it goes straight because it gives the impression it’s staying consistent with inflation and not buying any more goods or services.

But, the value of your debt is going down!

You're repaying the debt with cheaper dollars that don't buy as many goods and services.

That’s not all, there’s a catch. What's going to disrupt the increase of purchasing power you have, by leveraging inflation, is the interest rate you have to pay on this debt.

Depending on the interest rate you have, and inflation, your purchasing power is going to level out.

Again, it all depends on what the inflation rate is, relative to your interest rate.

If your interest rate is 3% and inflation over time has gone up by 6%, then the spread between the 3 and the 6 is increased purchasing power to you.

However, if your interest payment was 3% and inflation did not go up at all, then you’re going to lose purchasing power in the long run.

Why? Because the amount of interest you’ll pay the bank will exceed the amount that your income went up, due to inflation.

the takeaway for method #2

In other words, the takeaway for method #2 is:

If inflation exceeds your interest rate, you are making money.

Consequently, you may also think, what about deflation?

It’s a very good point, because deflation has the opposite effect of inflation, in the sense it makes the debt more expensive.

The good news is if you use these strategies in the correct location, even with deflation you will still do well.

I'll explain this further in the next method.

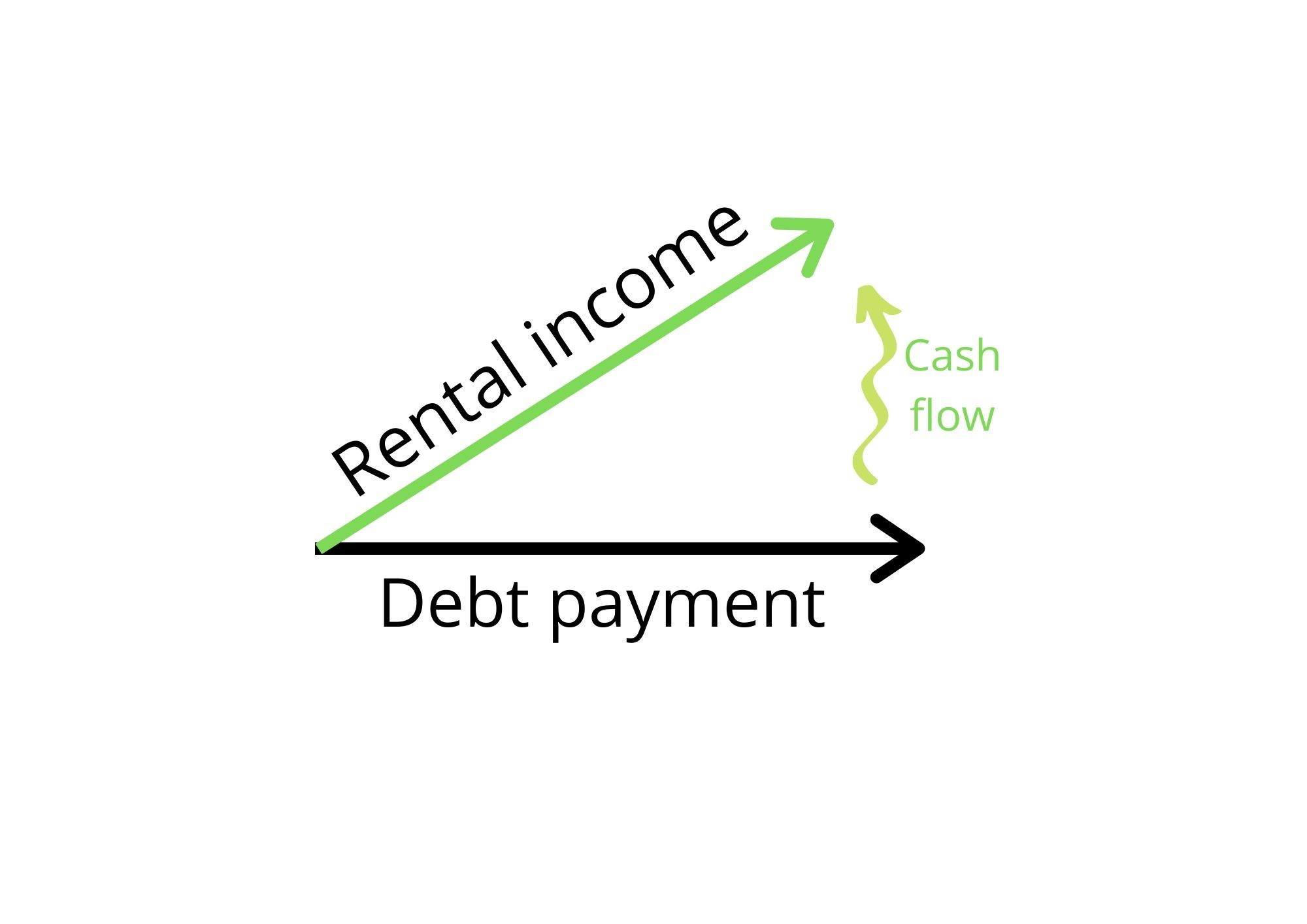

Method #3 (Cashflow Positive Rentals) – Shorting the Dollar with 30-Year Fixed-Rate Debt

Number three is owning cash flow positive rental properties with 30-year fixed-rate debt.

I am going to use the exact same figure I used in the last image, but in this one, as you can see in the image, we have a straight line for debt payments and a green one for rental income.

In this case as inflation increases so does our rental income.

Before I continue, I want to clarify something.

The debt payments in the drawing are the principal payments. It doesn't include interest.

Your first reaction to this might be: “well… those interest payments might cut into my cash flow, so it really depends on the interest rate I have, and the rate of inflation.”

Yet, it’s not true. Let’s think about it a little bit more…

Your renters are paying the interest rate.

This means that if the interest payments would normally cut into your increase of purchasing power with a house, where you live, with a rental property it wouldn’t because it’s completely paid for by your tenants.

The total discrepancy between the increases in rents and the payments of the debt are all additional cash flow in your pocket.

Moreover, it’s true your rental income would most likely go down if the economy went into deflation, and your debt payments would most likely stay the same.

This means the difference between your debt payments and your rental income would most likely decrease.

Still, let’s take it one step further.

If the economy did go into deflation, what would most likely also happen is interest rates would go down.

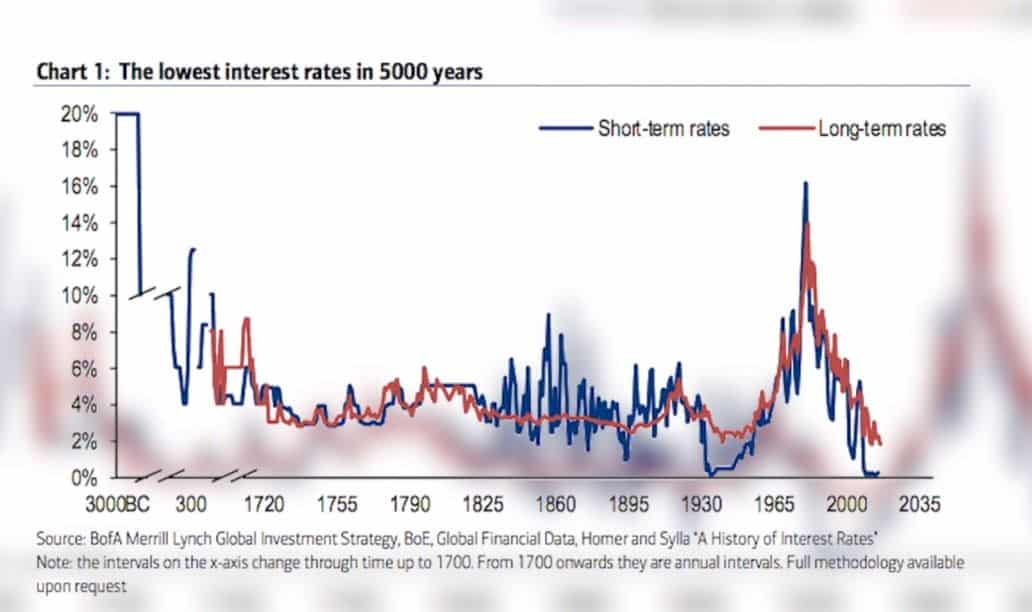

Now, I'm not saying bet on this because interest rates right now are 5,000-year lows. The chances of them going any lower are extremely slim, in my opinion.

Nevertheless, it’s a possibility. So, if interest rates went down, in this scenario, you could refinance your original loan and hopefully, get the loan to move in the opposite trajectory.

The differential between your income and your debt payments would remain the same.

It’s not for sure like it’s on the inflation side, but it gives you an opportunity to potentially hedge.

Furthermore, there are some areas in the United States where you completely want to avoid buying, even with a 30-year fixed-rate debt.

Real Estate Investing Cities To Avoid

San Francisco, Los Angeles, Portland, and Seattle.

There are others out there, but these are the big ones.

Because of the extremely high prices, historically speaking, and relative to inflation.

In addition to really bad government policies such as high taxes and rent control.

Another reason is they are based on asset prices, so if asset prices go down, meaning the stock market crashes, you are going to see real-estate prices, especially in areas like San Francisco, really struggle.

Same thing with interest rates. If you see the interest rate cycle start to reverse and go up for the next 20-30 years in certain areas, these are going to have big problems because the prices are very high and there’s so much debt in the system.

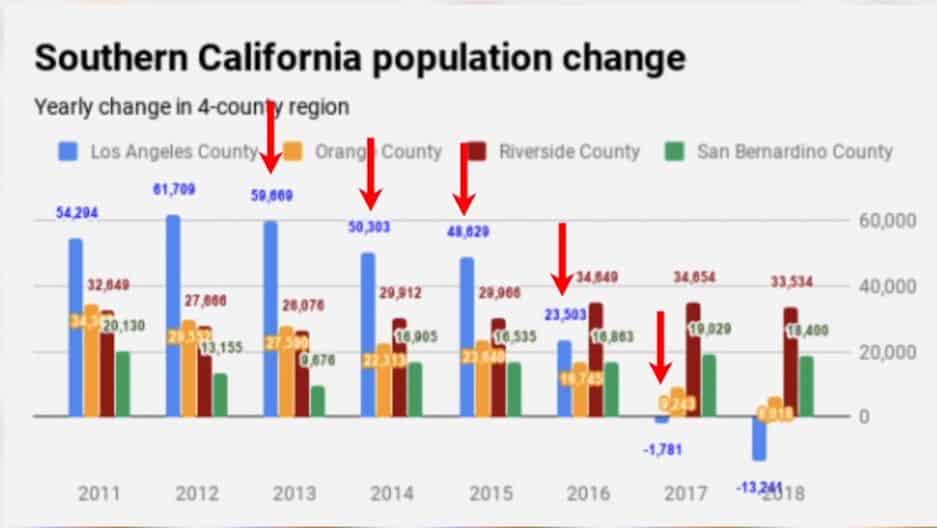

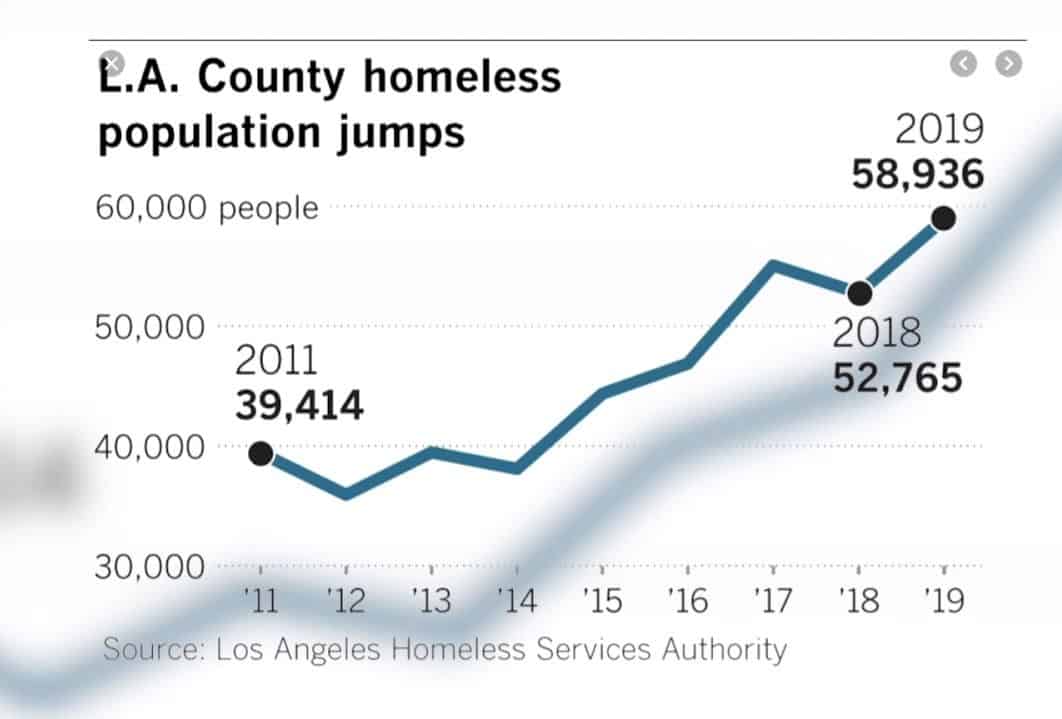

In some of these, especially in Los Angeles, the population increases are decreasing.

The amount of increase has been steadily shrinking, so by the time we get to 2021, you might even see the population decrease in the state of California, especially in areas like Los Angeles.

Also, a lot of these areas have terrible homeless problems. If you see a city with this problem, you really want to avoid it.

These are areas where you should buy in order to profit from inflation

Kansas City, Nashville, and Little Rock.

Why should you buy in these types of areas?

Because prices are much much lower, historically speaking adjusted for inflation, they have much better government policies and are not connected to asset prices.

Although they are connected to interest rates, they are not as heavily tied to interest rates because there is a lot less debt in those markets, and the population is gradually increasing.

If you want to know whether you should or shouldn’t buy, specifically in your area, you can also read this article where I go over a formula that will help you quantify and make better decisions.