Federal Reserve Balance Sheet

The dollar outside the United States keeps appreciating, gold is till plummeting and the Fed throws at us its latest bomb: They’re starting a $125 billion of quantitative easing per day. Yes, per day.

To give you a context, QE3 was $85 billion per month! And they just announced they will be doing $125 billion a day!

I frequently ask myself, where are they getting enough treasuries to buy?

The whole problem with the repo market or one of the main problems is there’s not enough collateral! So the Fed is out there taking collateral out of the system and putting it on to their balance sheet.

This is truly QE infinity. In fact, they’ve admitted it now, they’re not calling it QE infinity but open-ended QE.

There’s no limit to the amount of money they’re going to print, and they also came out with the statement they’re now buying everything.

They’re not pretending anymore, they’ve even extended it to student loans, credit card debt, auto loans, SBA loans, and my favorites, mortgage-backed securities, and commercial real estate.

Please look at what they’re doing.

They’re buying any asset class that can possibly go down, taking it off the private sector’s balance sheet and putting it on to theirs.

So no matter how much of a haircut these assets take, it’s not going to matter because its on the Fed’s balance sheet.

That’s today’s context, but my purpose with this article is to explain how is the price of gold affected so you can better understand why today is going down, and why is the dollar going up and its consequences.

Let’s start with why gold is going down.

Gold prices explained

The first thing we have to understand here is how a margin call works.

To do so I will give you an example.

If you buy $100,000 of stock margin, you only need to pay $50,000, but if the stock drops to $60,000, you’ve lost $40,000.

This means you now only have $10,000 in your margin account and the rules say you need to have 25% of the $60,000, so you have to deposit another $5,000 or you would have to sell another $20,000 worth of a share.

Usually, investors keep doing this over and over again if the market continually goes down until they’re broke.

This is the reason why you always hear people talking about liquidity and margin calls.

When the stock market goes down, they’ve got to raise cash very quickly, and a lot of times they do it going into the repo market.

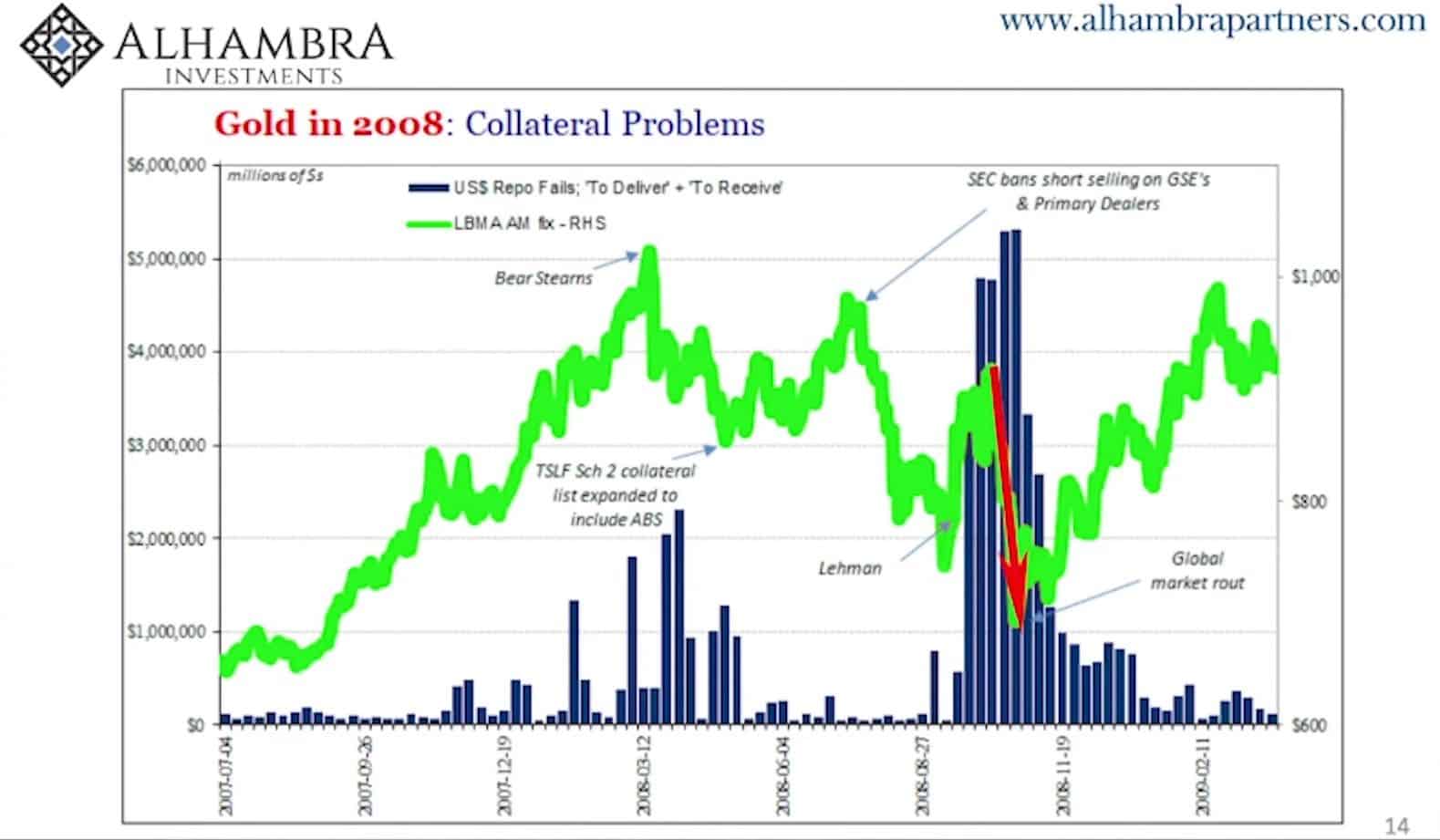

This brings us to a chart Jeff Snider gave me, please keep it in you're mind because I will point to it from now on:

This chart dates back to 2007 and 2008, on the left-hand side we have one trillion up to six trillion dollars, the green line is the price of gold, and its prices are on the right-hand side. The blue line represents the repo fails.

Repo fails are the transactions that fail to happen because one of the counterparties backs out a few minutes before closing the deal. There are several reasons for this to happen, but as the market gets shakier, usually you see more repo fails.

A repo fail would require one of the counterparties, for example, a hedge fund, needing the liquidity to meet the margin call, to sell something in order to generate the cash needed because they can’t get it in the repo market.

What would they sell? Something like gold.

In this type of situation, there are three cross-currents at play: Fear, liquidity, and collateral.

Going back to the chart, the blue line represents the collateral and the green line represents what’s happening with the price of gold in relation to fear, liquidity and collateral.

Starting in 2007, there was a lot of fear because of what was happening in the housing market, so gold went up almost in a straight line until we got to Bear Stearns.

Bear Stearns went bankrupt in the collateral issue and the repo market went through the roof.

As you can see, the repo fails reached its maximum after Bear Stearns went bankrupt, meaning, when the market was being shaky due to the collateral issue.

This means there was more liquidity needed for the hedge funds and financial institutions, so they had to sell their gold.

Therefore, the price of gold went all the way down util more collateral hit the market in the form of the government allowing or the Fed allowing asset-backed securities as collateral.

Once they temporarily fix the collateral issues, fear, once again, took over as the strongest cross current and took the price of gold up until they banned short selling on the GSE’s, then all of the sudden there’s was no more fear in the market.

Everyone thought the problem was solved, so the gold price went down until we got to Lehman Brothers, when fear took the lead again and the price of gold skyrocketed until the other two cross-currents, liquidity and collateral took over the amount of fear.

This caused the price of gold to plummet all the way down while the market was crashing until the Fed started QE1.

This put a band-aid over the collateral issue, but then fundamentals and fear took back over because the market saw how much money the Fed was going to print and how much the balance sheet was going to expand.

Gold, as a consequence, went on a bull run for the next two to three years.

So if we look at the repo fails, we can get a glimpse into what institutional investors were doing, and it helps us to better understand, not only why the price of gold is going down, but more importantly, when will it go back up.

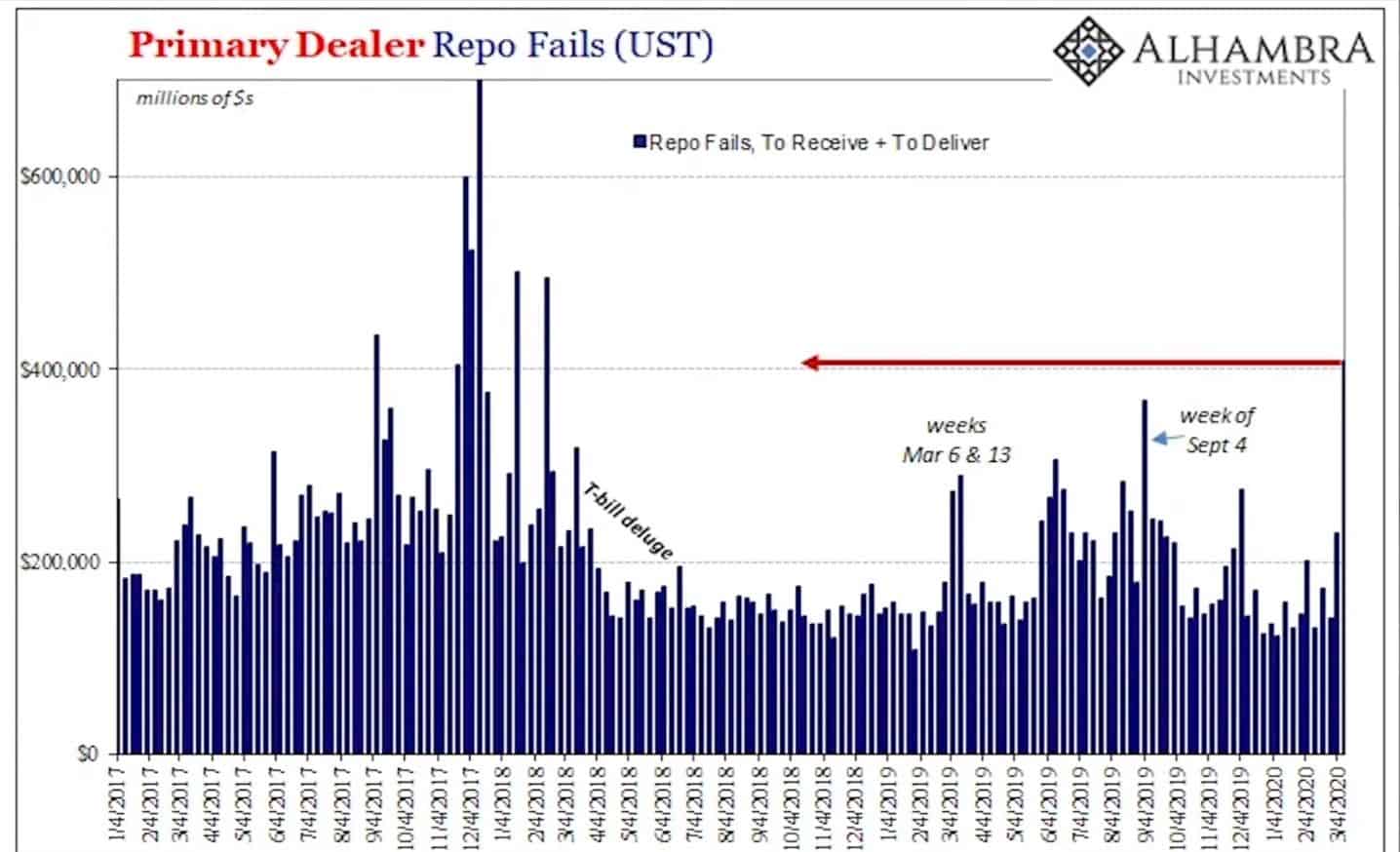

Let’s take a look at another chart from Jeff Snider to we can better understand the repo fails.

In this chart, you can see the current repo fails. Just going back to March 4th week, you can see the repo fails spiked dramatically.

So if this is a Lehman Brothers moment, we’re just at the very beginning, and we’d have to look at a chart of more recent repo fails to see if it’s increasing.

My guess of why this is happening is because the market, as we all know, is crashing.

So when the repo fails spike and then start to go back down, its because institutional investors will have either sold all their gold, meaning they don’t have anything else to sell, or the Fed somehow, temporarily solved the collateral issue once again in the dollar funding markets.

With this, I’m by no means saying you should base your decision on whether or not to buy gold for your portfolio on the repo market or repo fails.

I’m only going over this so you can get a better understanding of what factors affect the price of gold.

Dollar price explained

Now, diving into the dollar rise, we need to be clear about something, the dollar is going up in value against a basket of other currencies. It doesn’t necessarily mean the dollar is going up in value relative to what you buy on a daily basis.

The currency could be going down in value for food and up in value against the Yen or the Euro.

It’s also very important we understand there are two completely separate economies for the United States dollar: The domestic and the international economy.

As we all know, the dollar is the world’s reserve currency, so is not only oil denominated in dollars, meaning you have to pay for oil in dollars regardless of the country, but most of the corporations outside the United States are funded in dollars as well.

For example, let’s say you’re a Canadian starting a gold mine in Brazil, you would most likely borrow dollars in order to start your business.

This means a lot of countries and entities outside of the United States borrow in dollars, this started to happen especially during 2012 and 2014 when the dollar was cheap and interest rates were zero like we have today.

Therefore, a lot of countries and corporations outside the U.S. loaded up on dollar-denominated debt even though their revenues were in their local currency.

What I mean by companies loaded up in dollar-denominated debt will be better understood with these charts:

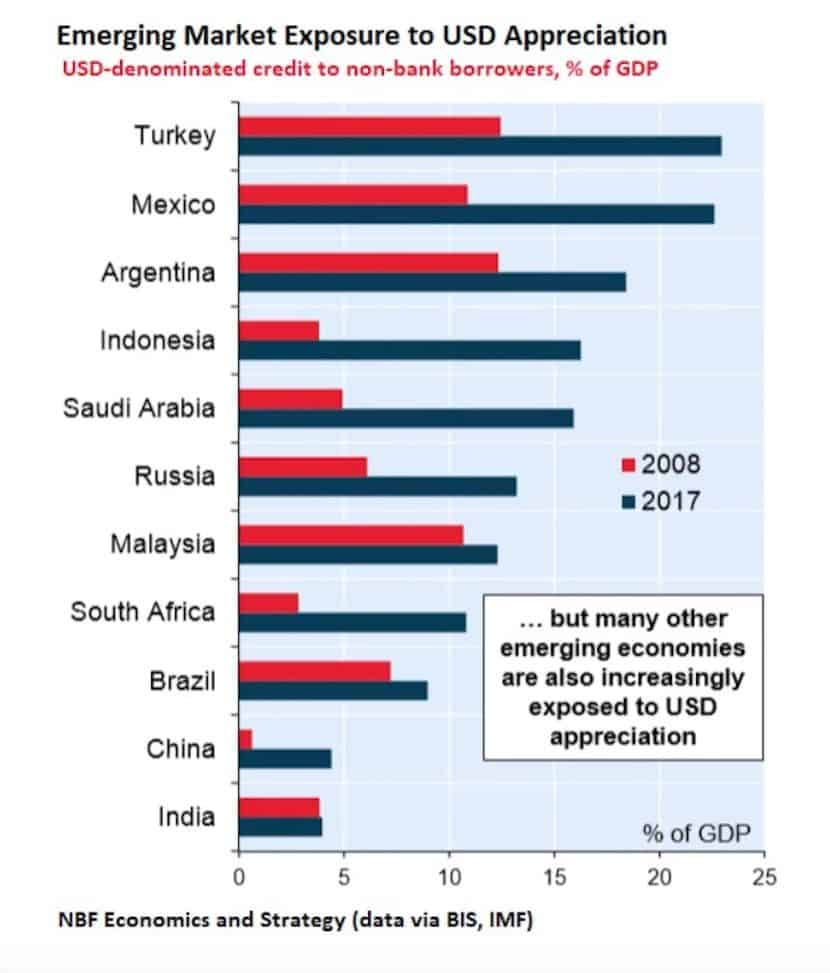

This is a great chart of emerging market exposure to USD appreciation.

What they mean by it is how much debt they have in dollars and how they’re susceptible to their currency losing value against the dollar.

For example, Turkey had dollar-denominated debt, as shown in the chart, for the amount of 13% of their GDP, as of 2017, the number changed to 24%.

Going down to Mexico in 2008, 11% of their GDP was in dollar-denominated debt, now, it’s 23%.

We can also see countries like Indonesia, Saudi Arabia, Russia, South Africa, and China have a huge difference, a massive increase in the amount of dollar-denominated debt they have relative to 2008.

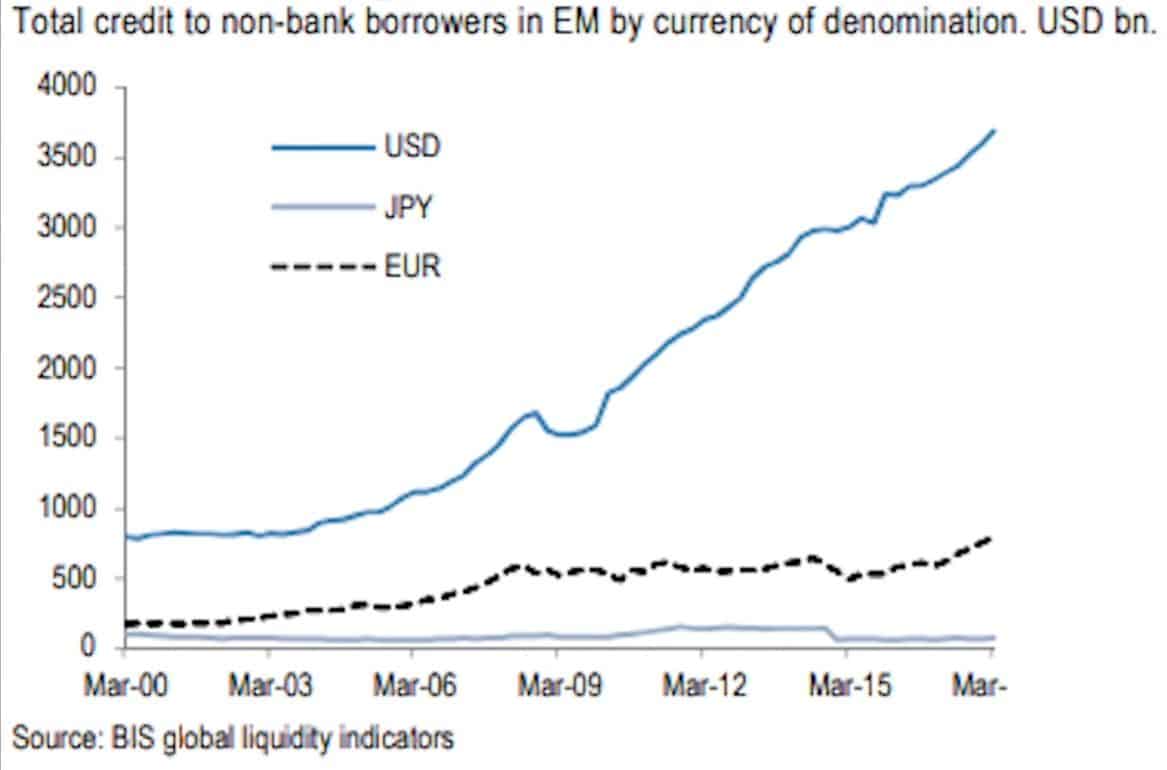

Here’s a second chart which gives us a great visual and specific numbers:

Look at how it flatlines from 2000 all the way to 2003 and 2004 and then it goes almost straight up to where we get to a point today where we have over $4 trillion in debt of only emerging markets.

This means the world in total has a lot more dollar-denominated debt than you see in this chart.

This is huge because most of this debt was taken on when the dollar was very cheap, about 70 on the DXY. Today, it’s over a hundred.

Think about what this does to the value of the debt when your revenue to pay the debt has gone down in value.

For example, if a country like Colombia or South Africa with a lot of dollar-denominated debt, gets its currency depreciated by 20%, unless they have some form of dollar-denominated revenue, in this case maybe oil, how would they make up the difference if not by printing money?

Add to this injury the insult of oil price going down.

The only way they can make up the difference is by printing more money, more than what they would’ve back in 2012 because the dollar since then appreciated.

Using real numbers, back in 2012, there was 1 peso for every dollar, now there are 2 pesos for every dollar, so if they had a thousand dollars in debt, now they have to print $2,000 instead of $1,000.

This creates an additional supply of the currency of whichever country we analyze, and the more money supply, the more the price goes down.

It’s also important to remember, because of what’s happening with the Covid-19, and the whole world going into recession, if not a depression, these countries can’t increase interest rates to defend their currency.

This, meaning their currency will come into a doom vortex where they can’t increase interest rates because it crashes the economy, but if they don’t it will lower the value of their currency, which would make them print more currency to satisfy the dollar-denominated debt.

It gets ugly very fast.

Before I continue I want to clarify this doesn’t just happen in countries where most Americans would consider third-world, this just happened in Australia where their currency took a beating against the U.S. dollar in a very short of time, as shown in the chart.

Why did this happen to them?

Because their economy is having significant problems, and the only thing they can do is print, but they can’t increase interest rates.

The important lesson here is other countries’ currencies go up and down based on the fundamentals of what’s happening domestically where the United States dollar is unique in the sense it doesn’t always go up or down with what’s happening domestically in the U.S economy, but more so with what’s happening outside of the U.S.A.

Can the Federal Reserve solve all problems?

What I mean by solve is put a temporary band-aid on it, because there’s no way they can permanently solve this issue.

The only thing that’s going to fix this is a reset of the entire system.

As I mentioned before, the Fed is literally buying everything.

This means the next time you go down to your local Subway if you’re not quarantined already, that strip mall could potentially be owned by the Federal Reserve.

But the important thing to remember aside from the insanity of what the Fed’s doing is the transaction between the primary dealers and the Fed doesn’t create additional deposits in the real economy because the primary dealers have accounts held with the Fed.

So if the Fed buys an asset from any primary dealer, or if any of them give the Fed an asset as collateral, the asset goes on to the asset side of the Fed’s balance sheet.

The Fed takes collateral or garbage collateral from its primary dealers and then crates funny money out of thin air and deposits it into their reserve accounts, this means there are no additional deposits available to spent other than by the primary dealers themselves.

However, this week’s announcement changed everything.

The Fed is going directly to all the other entities outside of their umbrella, meaning hedge funds, corporations, financial institutions and most likely the general public, the small and mid-size businesses.

They’re starting helicopter money or MMT, or at least I think it will be the Fed’s next step.

But again, the difference between the Fed’s relationship with its primary dealers and with all the other entities is the first one only creates more deposits in the Fed’s reverses, while the other relationship creates more deposits in the real economy.

To understand how it works here’s an example.

The Fed comes in and takes a $1 billion dollar worth of consumer credit card debt off a retail bank’s balance sheet, and in exchange for it, the Fed deposits $1 billion in the retail bank account.

The retail bank account will consequently go up by $1 billion increasing, this way, deposits in the real economy.

But then, to offset the liability, because it becomes one on the balance sheet of the retail bank, the Fed prints up more money and adds it to the reserve account of the retail bank.

It’s still just printing up reserves and putting it on the Fed’s balance sheet, but in the case of the primary dealers, just to reiterate, it doesn’t create and additional deposit at a retail bank.

So if it creates a deposit with a retail bank, it’s increasing the money supply, or, the same money chasing the same amount of goods and services.

If velocity stays consistent or increases, we would have consumer price inflation domestically.

My point on going over this question is to show you that as far as the collateral problem or the liquidity problem goes, inflation could be an issue to bring the gold price down further like we saw in 2008 with the repo fails spiking.

After seeing this and what the Fed decided on Monday, I can conclude maybe the repo fails are at a maximum right now.

Maybe, from now on they’re going to go down because how could there be a liquidity problem or a collateral problem anymore when the Fed has literally exchanged all the existing collateral for liquidity?

I’m going to call Jeff Snider and see if I can book an interview with him or something so he can tell me where I’m wrong, but I think this could solve, temporarily, the problem of liquidity and collateral.

This way, fear, and fundamentals might take over and we could see the gold market going back up.

But, in this overview, I don’t want you to miss the problem of the dollar outside the U.S.

The dollar outside the U.S.

The government is going to deficit spend and they might just spend as much money as the Fed, the difference is the government can’t print funny money out of thin air, like the Fed, rather, they have to issue debt.

So they would have to issue new treasuries causing interest rates to go up, which means the Fed has to monetize the debt by buying a lot of those treasuries.

Therefore, the treasuries would go from the government by auctioning them off, on to the Fed’s balance sheet, then the Fed would have to print more money and deposit it into the treasury general account.

From the treasury general account, the money will go into the economy because the government will be spending it.

So those dollars come raining down on everyone in the real economy.

But, the problem we’re talking about is dollars outside the U.S., not inside, so how do dollars get outside the U.S.?

There a lot of different ways, but the main one is by the country importing more goods and services than exporting them. That creates a trade deficit.

But, since we’re buying more goods and services from other countries, the only thing we have to give in exchange for them are little green pieces of paper.

All those dollars come out of the United States and into other countries and the imports come into the United States. This is usually how the world gets the dollars they need.

However, we have to insert Covid-19 sickness.

We all know global supply chains are being disrupted, which means fewer imports are coming into the United States and fewer exports of dollars are going out of the U.S.

With this kind of situation, I think is very possible, nothing is a certainty, especially these days where all is uncertain, I mean I didn’t know I would wake up a morning to hear the Fed announce QE infinity, but I could see a very possible situation play out.

The dollar outside of the United States can continue to go up in value while at the same time, inflation on staple goods, meaning all the products we import from China and sell at Walmart, Home Depot, and Target, will go up in price and gold will follow.

This is very counterintuitive but we are living in very strange times, so I’m not saying this will happen, but I am saying it is probable and we should, therefore, think about how it would work, and be financially prepared.