An Actionable 100 Year Analysis Of The S&P 500

The returns that normal people care about, and the amount their investment actually grew, gets measured by CAGR (compound annual growth rate).

Let's explore this and try to discover which approach yields the highest CAGR over the long haul. Then let's see where real estate fit's into the equation

To analyze the best strategy to maximize returns I compared several approaches.

1. Interest rate cycles.

As we all know, interest rates are cyclical, and they run in very long cycles of 20 -30 years.

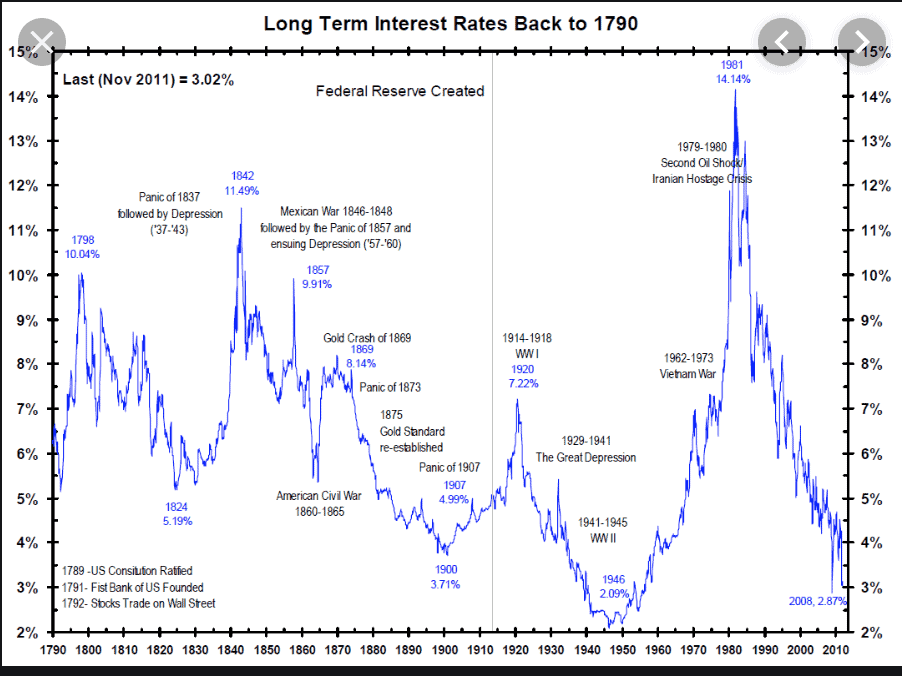

I found data for interest rates going back to 1790 but could only find CAGR for the market going back to 1871 so that's where I started.

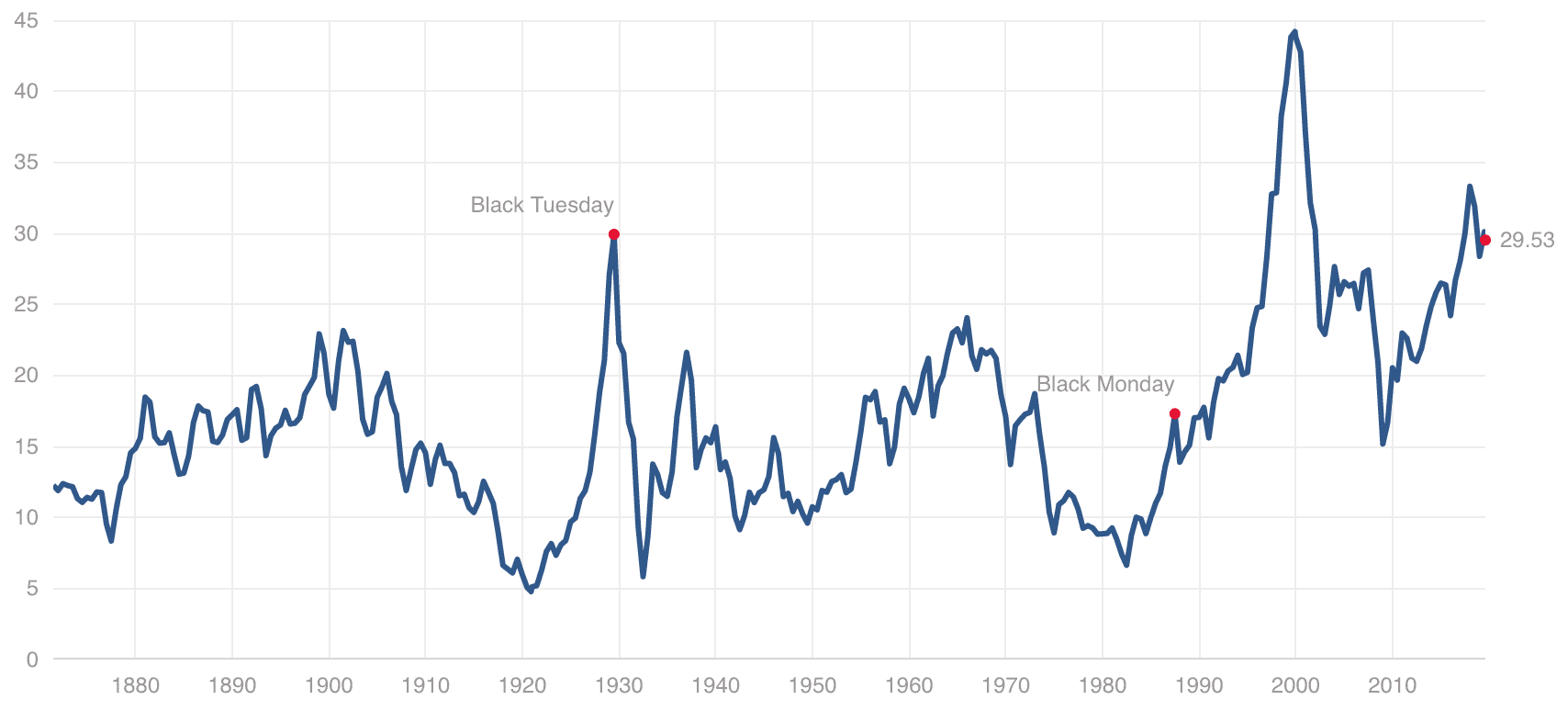

Here's the chart of interest rates I used.

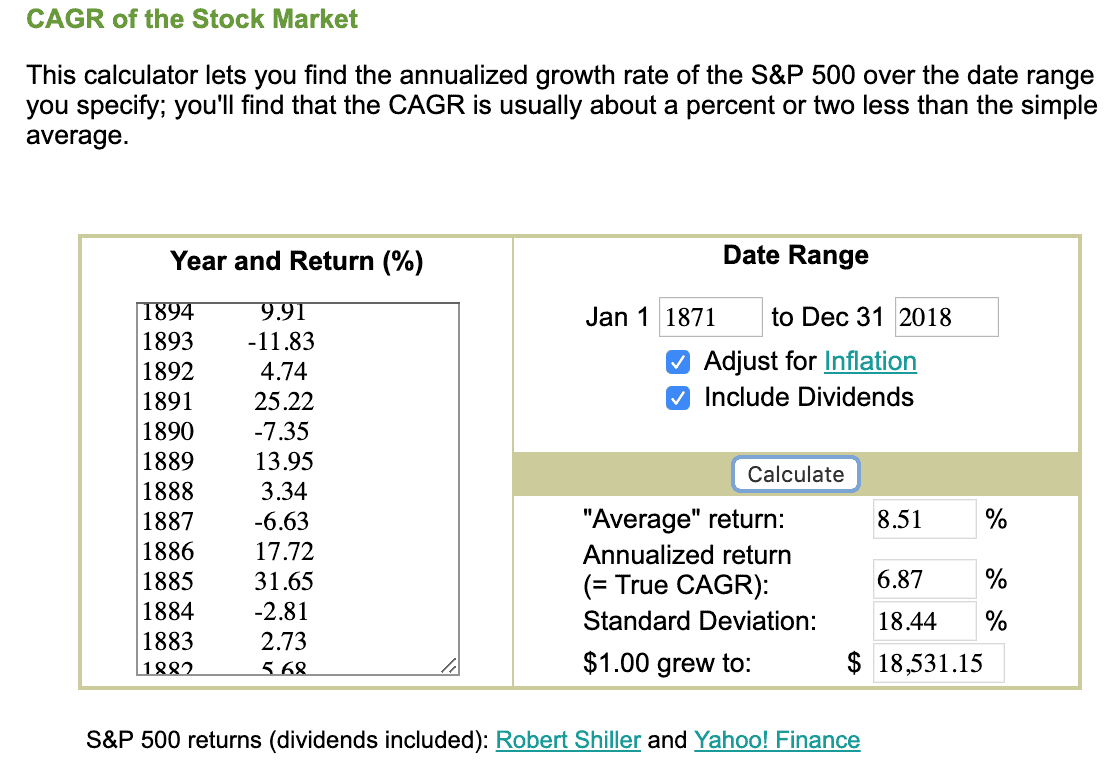

I took each time frame of rates going up and down and plugged those into the CAGR calculator (I included dividends and adjusted for inflation).

Here's a screenshot of the calculator (below).

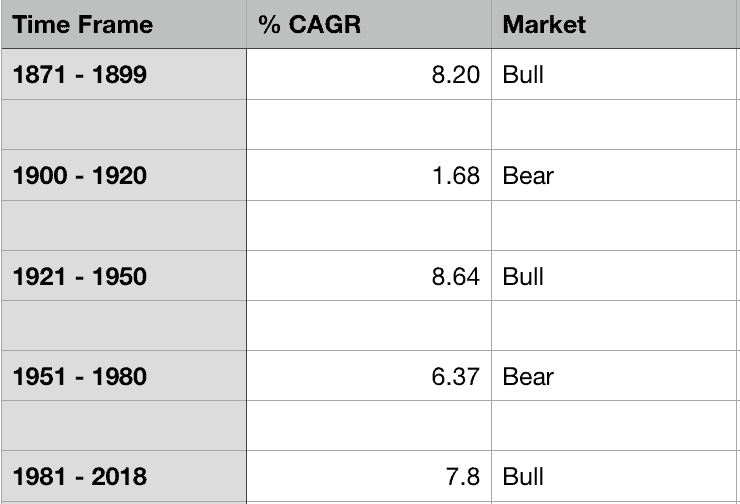

And here are the results.

As you can see, there was a difference, during interest rate downtrends the S&P performed better.

Unfortunately, it wasn't a significant enough difference to suggest waiting for the start of another down cycle in rates to start investing, your cash would be an idol for too long eliminating the edge, creating a lower total compounded growth rate.

At best I think this is a broad predictor of future expected returns based on current P/E multiples and where we are in the cycle.

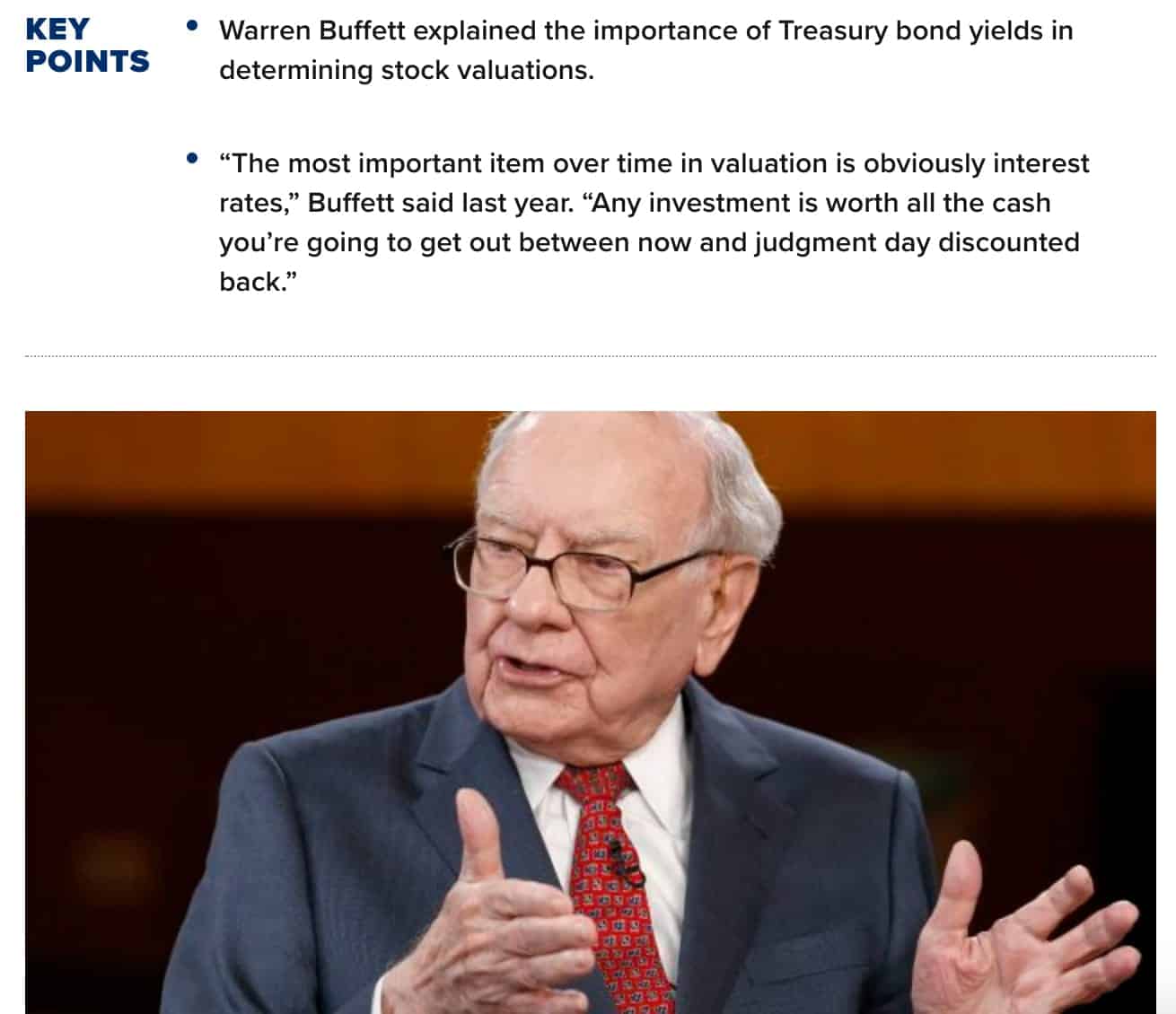

This makes sense because a stock is a claim on future cash flows and interest rates are a discount mechanism for future cash flows.

Here's Warren Buffet commenting on this.

Again, the simple takeaway is, down cycles in rates will create a tailwind for stock prices, upcycles in rates will create a headwind for stock prices.

A quick observation of where we are in an interest rate cycle can assist in predicting if future returns will be higher or lower than the historic norm (going back to 1871).

FYI, we're 40 years into an interest rate down cycle…

2. Backtest strategy using lows in Shiller P/E ratios.

My hypothesis was investing only when P/E ratios where at their low would give enough of an edge to make it a useful strategy.

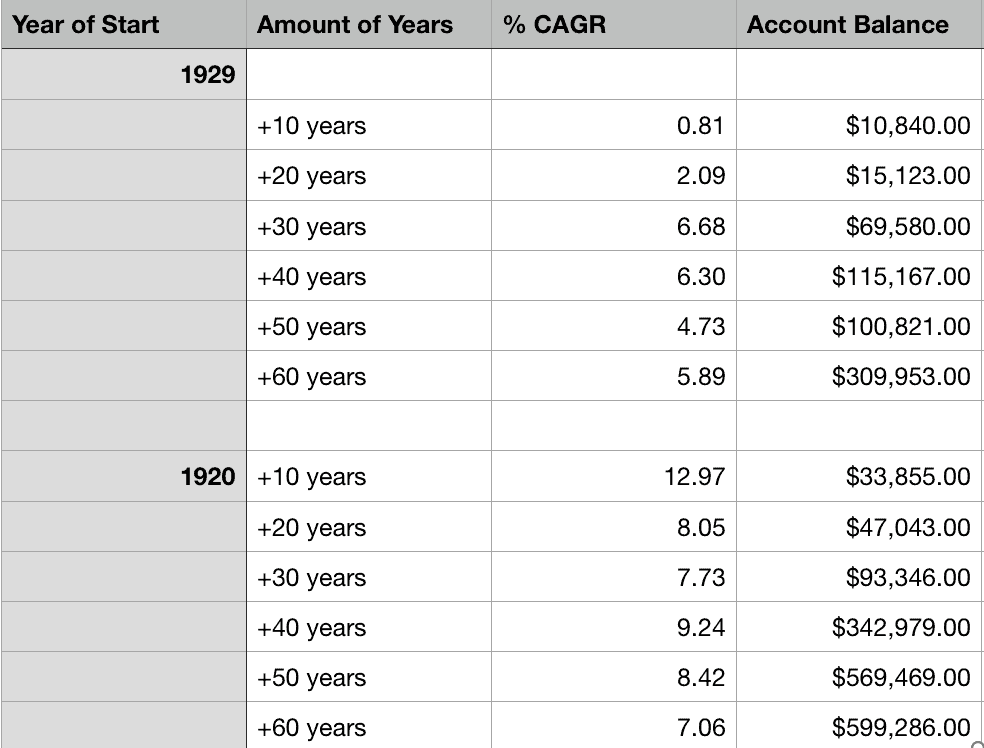

To test this I used two dates as starting points, 1920 (an absolute low in P/E' ratios) and 1929 (a high in P/E's close enough to do decades-long tests). Here's the chart

Please note the difference in P/E's between 1920 and 1929 (above).

Here my results assuming a starting investment of $10,000, adding dividends, and adjusting for inflation (below).

After each 10-year time frame buying from a low starting point massively outperformed.

But is it realistic for most, who only have roughly 35 years to save, to wait for the next time P/E's go to 5?

Obviously not.

Although this didn't give us an investable strategy it did show that, if possible to deploy, “buy low” works.

You may be saying “Duh George.”

But remember, the collective ethos is “buy always.”

What's the saying real estate agents have?

“Don't wait to buy real estate, buy real estate, and wait?” I'm sure financial planners have a similar saying. 😉

3. Only buy when P/E's are low, not necessarily at their all-time lows.

My next hypothesis was narrowing the wait time to buy.

I wanted to buy when P/E's were below 10 and sell when P/E's were above 20.

In the interim, sit on the cash.

This is very consistent with my RE strategy, which is buy when it's historically cheap, and sell when it's historically high.

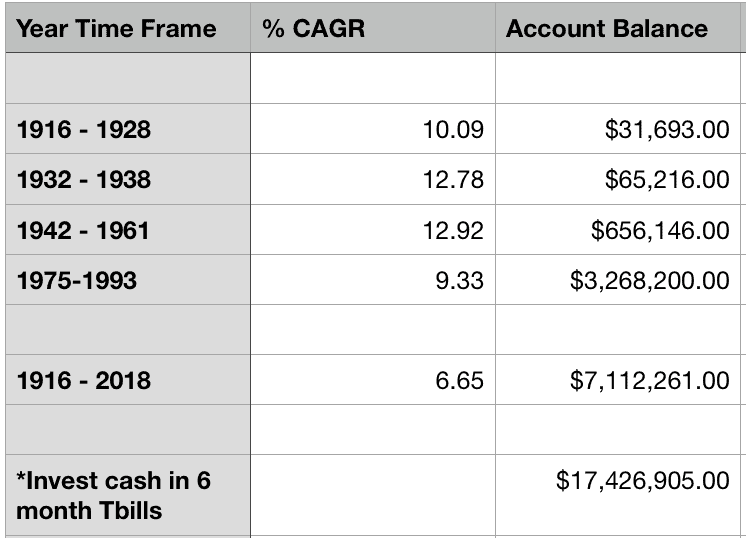

Let's check out the results, again starting with $10,000, adding dividends and adjusting for inflation.

The time frames coincide with the points on the Shiller P/E ratio chart above. Remember, buy when P/E's dip below 10 and sell when they go above 20. (I accidentally left out 1878 – 1898 it was 9.8%)

It worked very well in the sense it gave us multiple entry points.

But did it work better than just buying in 1916 and leaving your money in until 2018? No.

It performed significantly worse (3.2 million compared with 7.1 million), because the strategy of buy under a P/E of 10 and sell at a P/E above 20 has been sitting on cash since 1993.

The big problem is the time between when you sell and when you buy…Maybe the numbers do favor those who “don't wait to buy, buy, and wait?”

4. Buy low, sell high, and but the cash in 6-month treasuries between high and low points.

For my last hypothesis, I wanted to see what would happen if we used my buy under 10 and sell over 20 approaches combined with putting the cash in 6-month treasuries (to lower inflation risk and provide liquidity without relying on the market value of the t-bill).

I couldn't find data going back to 1916 for 6-month t-bills, but what I found showed a rough average of 3% in rate bull markets and 6% in rate bear markets.

I plugged those values into the times the strategy was in cash. The results are on the spreadsheet above.

Using this method, starting with $10,000 in 1916, including dividends, adjusted for inflation, at the end of 2018 you'd have $17,426,905.

Compared to $7,112,261 with the traditional buy and hold method.

If we're strictly measuring long periods of time, as Dave Ramsey does, the buy low, sell high and keep your cash in short term treasuries vastly outperforms.

More importantly, it's something any average Joe can do.

So what about REAL ESTATE??

Bad news fellow real estate investors.

Going back 100 years, comparing decade to decade, if you keep your money in the market 20-30-40 years, the market outperforms (including dividends, adjusted for inflation, NOT including leverage or taxes).

Why? The same reason all the strategies above, except the last, underperformed.

Cash, or in this case cash and equity, sit idol too long without the effects of being compounded.

Additionally, rents and prices don't really go up, they only keep pace with inflation.

True, both have periods of time when they wildly exceed inflation (like right now) but going back to 1890 they've always mean reverted.

Which makes sense because they're a direct function of real wages…stocks are not.

It is true, real estate provides much better cash on cash return

I'm sure most investors can get at least a 7% cash flow without leverage.

The problem is the amount of time you have to save up that cash flow, or build equity via mortgage payments, to make another investment and start compounding the money.

Did I do a spreadsheet for Real Estate? No.

I didn't need to because doing the homework for the other strategies I knew a 10% yield would never outperform a 7% CAGR unless the money from the yield was constantly being reinvented with the same yield.

Not reinvested once every 2-10 years pending on inflation or real appreciation etc. (to extract and reinvest equity/cash flow).

NOTE: I did not factor in leverage and taxes to keep a more apples to apples comparison. We all know those 2 factors are huge.

But wait, I have good news!

There is one area where real estate will almost always outperform stocks.

In 2019, when there's $15 trillion in negative-yielding debt in the world, the USD is losing its grip on world hegemony, US $23 trillion in debt with $100 trillion in unfunded liabilities, the largest debtor nation in world history…I could go on and on.

What's more important CAGR or capital preservation?

I'd argue capital preservation. And in that arena, Real Estate is the champ.

As we all know, prior to 2006 the Real Estate market had never gone down in nominal terms.

Even when the bubble burst prices went down by 60% to the market 50%.

Not a big enough difference to make up for the countless times over the last 100 years the market has dropped massively.

The bottom line is Real Estate is far less volatile.

And in a world with macroeconomic conditions as they are today that should take precedence.

If you've read this far I sincerely thank you.

I know this is a ridiculously long post but I strongly believe the information is of value because it's so rare to see details and actual data. I think the in-depth analysis is the cornerstone of good investment decision making.

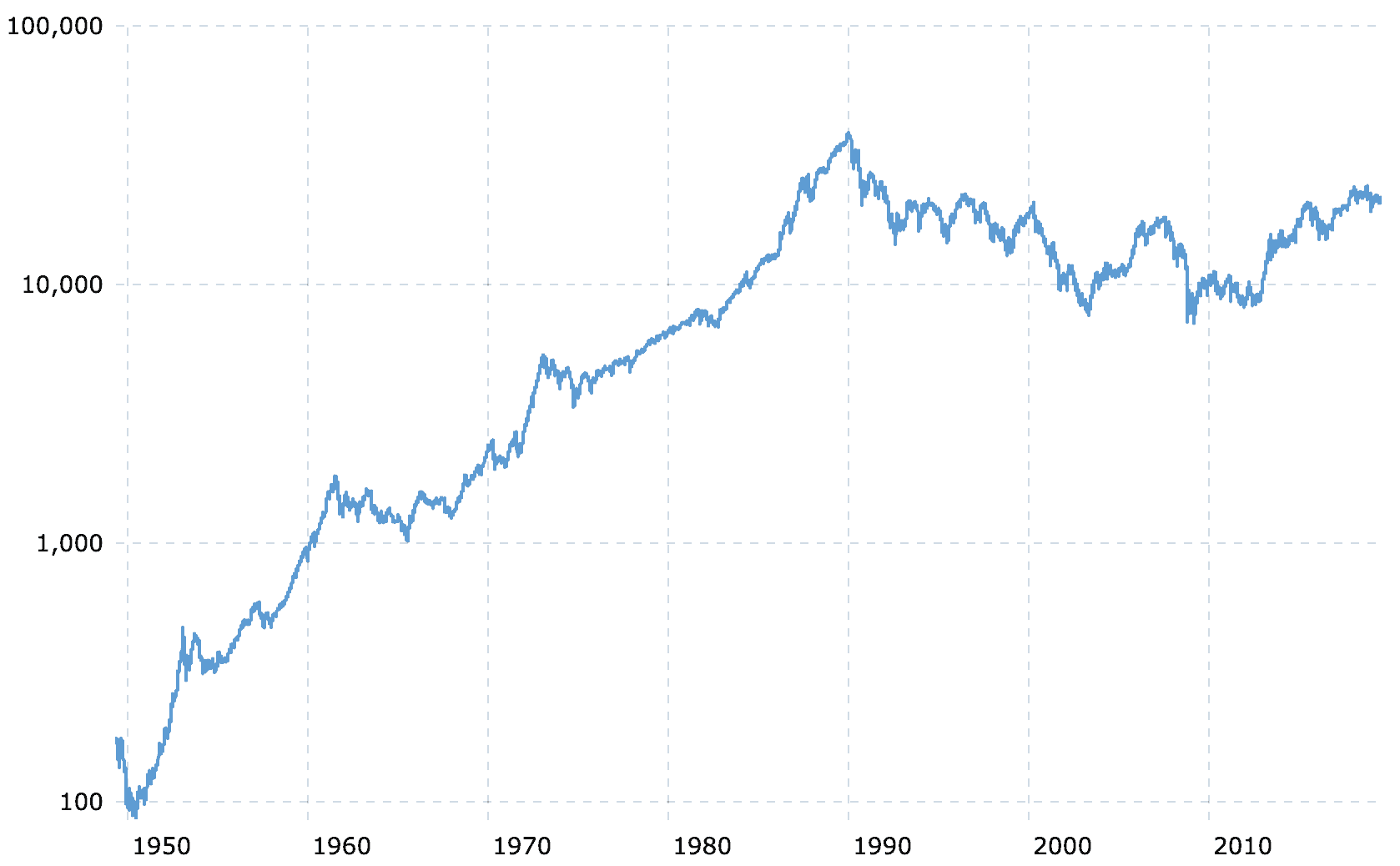

That said, let me leave you with a chart from Japan's Nikkei index as a further counterbalance for stocks having a higher CAGR over the long haul.

Notice where the Nikkei was in 1989 and where it is today, 30 years later…lower.

In fact, it never got close to the 1989 level again.

Why couldn't the US be the next Japan?

If you give me 3 reasons their economy is worse, I can give you 3 reasons it's better.

And remember, Japan is the largest creditor in the world, the US is the largest debtor in the history of the world.

All the results I've given you in this post are from the past, as we all know, the past isn't necessarily a predictor of future events.

If we all lived in Japan in 1989 and made investment decisions based on the last 40 years how well would we of done in the future?

Takeaways:

1. Buying the S&P under 10 (Schiller P/E) and selling over 20 and buying short term t-bills in the interim yielded the best results for stock market investors.

2. Real estate is a superior way to preserve cash flow and short term cash flows are much higher.

3. All of these assumptions are based on past results, which as Japan teaches us, are not always indicative of future results.

George.